Implications for cost management analysis of new green building materials in the context of low-carbon economy: a critical review in China

*Correspondence to:

Ming Zhang, School of Management, Guangdong Ocean University, NO.1 Haida Road, Mazhang District, Zhanjiang 524088, Guangdong, China.

E-mail: zhangming314@163.com

J Build Des Environ. 2024;2:32646. 10.37155/2811-0730-0302-13

Received: May 06, 2024Accepted: June 20, 2024Published: July 01, 2024

This article belongs to the Special lssue Innovations in Low-Carbon Construction Materials and Engineering

Abstract

The Chinese government vowed to achieve “carbon peak and carbon neutrality” on a global scale in 2020. Since the building sector emits a significant amount of greenhouse gases, achieving the “carbon peak and carbon neutrality” goal will be extremely difficult. Emissions of greenhouse gases can be greatly decreased by developing low-carbon buildings. As more and more new green building materials hit the market, China’s low-carbon construction sector is growing along with the building materials market. This study does a thorough analysis of the literature on the most recent advancements in cost management related to new eco-friendly construction materials in low-carbon economies. The objective is to describe the different dimensions of information green building materials cost management, uncover the underlying themes and sub-themes within these dimensions, identify key research gaps in the current studies, and provide recommendations for future research endeavors. Through the review of the literature, the existing problems in the cost management of new green building materials are revealed. And from the improvement of new green building materials cost management way is elaborated. The conclusion of this paper is that the existing research mainly focuses on the construction of cost management systems and does not systematically study the formation process of material costs, ignoring the consideration of material research and development technology, environmental accounting disclosure and other aspects. Finally, the research project ought to prioritize material research and development, strengthening the cost accounting system, environmental cost disclosure, improving the material management system, and other areas that require in-depth investigation.

Keywords

Low-carbon economy, new green building materials, cost of building materials, cost management

1. Introduction

Urban building is growing rapidly in tandem with China’s urbanization trend. As part of its goal to reach “carbon peak and carbon neutrality”, China has made the shift to a low-carbon economy with sustainable energy and economic structures as a central focus for future economic growth.

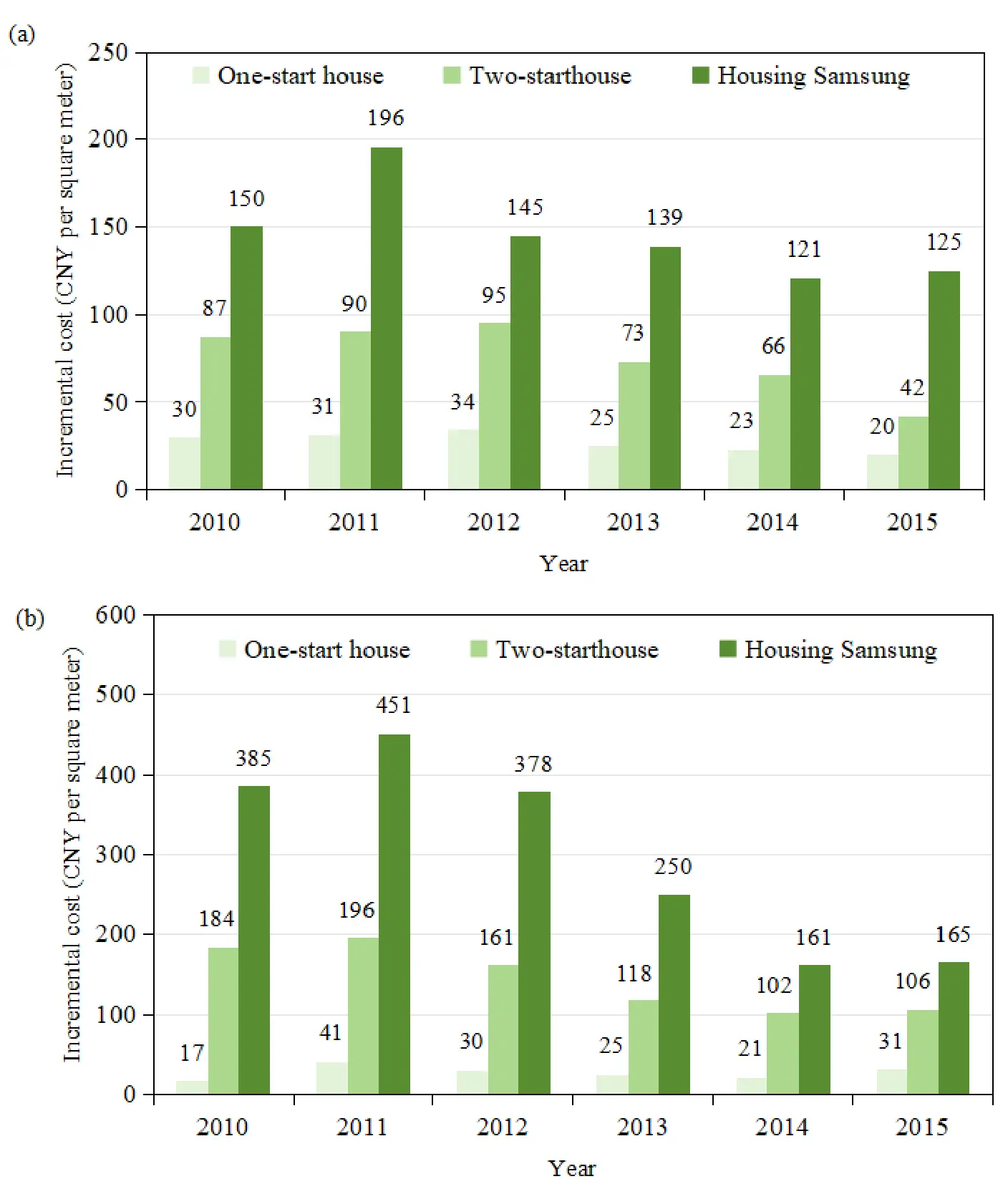

The economic structure of construction enterprises has also gradually changed from extensive to intensive, with the continuous development of China’s low-carbon economy[1]. In 2021, the “Opinions of the Central Committee of the Communist Party of China and the State Council on Fully Accurately and Comprehensively Implementing the New Development Concepts to Do a Good Job of Carbon Peak and Carbon Neutrality” contained a proposal by China’s General Office of the State Council to actively develop energy-efficient and low-carbon buildings as well as to comprehensively promote green and low-carbon building materials. When compared to conventional building materials, new green materials have the green attributes of being healthier, more environmentally friendly, and requiring less resources[2]. Therefore, the issues of excessive energy consumption and emissions in the construction industry can be significantly mitigated by the use of innovative green building materials. It may also encourage the building sector’s growth in a low-carbon, environmentally friendly, and sustainable manner[3]. In the discipline of construction engineering, the cost of building supplies makes up over half of the whole expenditure[4]. However, with the advancement of green building principles like “Passive Technology Priority and Active Technology Optimization”, a variety of green building material technologies that boast low incremental costs, excellent regional adaptability, and well-established technical systems have gained traction in the market. This trend has resulted in a decrease in the incremental costs associated with green buildings (Figure 1).

Figure 1. Changes in the cost of China’s green building labeling program over the years[1]. (a) Residential building; (b) Public building. CNY: Chinese Yuan.

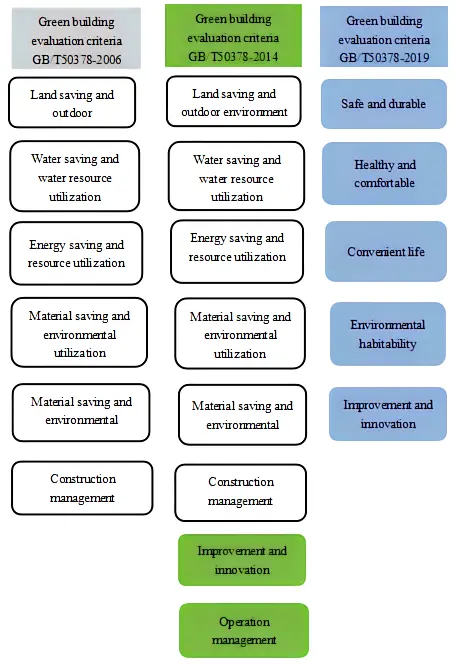

The reduction of incremental cost of green buildings is due to the continuous improvement of green building evaluation standards in China. China’s first ecological housing evaluation standard, the “China Ecological Housing Evaluation Standard”, was completed in 2001 by academics from China. It was developed by combining China’s actual development situation with extensive research and discussion on green ecological building housing industry technology in other countries. In 2003, to support the Green Olympics and fulfill the promise of the “Green Olympics”, under the guidance of Tsinghua University, the Beijing Science and Technology Commission formulated the “Green Olympic Building Evaluation System”, which is the first green evaluation standard system launched in China. China updated and enhanced the Green Building Assessment Standards in 2006[5], 2014[6] and 2019[7]. The 2014 edition’s category evaluation indexes are more “construction management” and “improvement and innovation” than the 2006 edition’s, as shown by comparing the versions of different periods (Figure 2), which is because the material saving and water saving during the construction period are also required, and additional points are set for new technologies. The evaluation object from the 2006 edition, which included public and residential structures in office buildings, malls, and hotel buildings, was enlarged to include all civil buildings in the 2014 edition. In contrast to the 2019 version. The 2014 edition has experienced significant modifications, with the amount of indicators being more condensed, simpler to comprehend, and easier to master, replacing the previous “four sections-environmental protection” with “five performances”. The development of “convenience of life” and “health and comfort” is increasingly focused on the needs of the individual, which is consistent with the national development strategy of promoting innovation in the new era and giving consideration to the shared advancement of efficiency and quality. Meanwhile, the index’s 2019 version categorizes green buildings into four fundamental levels: basic, one-star, two-star, and three-star. The five indices that make up the green building evaluation index system are resource-saving, livable environment, convenience of living, health and comfort, and safety and durability. In order to encourage more construction companies to move toward low-carbon, environmentally friendly construction, use more green building materials, lower the incremental cost of construction projects, and increase economic benefits, evaluation standards can be developed to support the integration of the concept of green development into building green development requirements.

In addition, financial subsidies from national and local governments have largely offset the incremental costs of green buildings. At the same time, a typical green building project can recoup the incremental cost of green technologies within five to ten years, with the exception of a few green building projects[7]. Therefore, the use of new green building materials can, to some extent, reduce material maintenance costs, reduce carbon emissions, increase material application rates and ultimately reduce material costs and overall costs[8]. Despite the progress made in the new green building materials industry, several challenges persist. These include imperfect market mechanisms, inadequate knowledge of new green building materials among managers, high production costs associated with these materials, and ongoing fluctuations in material prices. These issues can have a substantial impact on cost accounting and management practices related to building materials, consequently influencing the construction efficiency of construction projects.

The green building star rating means that green buildings should meet the requirements of all control items of this standard, and the score of each index should not be less than 30% of the full score of its score item. When the total score reaches 60 points, 70 points, or 85 points and should meet the corresponding technical requirements of green buildings, the green building grade is one star, two stars, or three stars[7].

Currently, both domestic and international scholars primarily concentrate on the low-carbon economy and its application in the realm of building materials cost management, with a specific focus on the market, design, construction, and overall management aspects.

Wu et al.[9] conducted a study on the low-carbon transformation of the construction industry with the aim of “carbon peak and carbon neutrality”. They highlighted that the production phase of building materials and the operational phase of buildings are pivotal stages for carbon emissions in the overall construction process. Subsequently, they proposed a “step-by-step” approach to facilitate the low-carbon transformation of the construction industry, emphasizing “systematic promotion, targeted policies, dual-pronged initiatives, and consistent, organized progress” to propel the high-quality development of China’s construction sector. Lin[10] identified the following problems in the cost management of building materials:

1. The quality inspection at the time of entry is not strict, and the management personnel do not procure materials according to the contract requirements.

2. Material storage is not in place, the storage personnel is easy to temporarily neglect, resulting in material damage, which further affects the quality of the project.

3. In order to control material costs, some enterprises have set up unreasonable procurement incentive mechanism, leading to the occurrence of counterfeit inferior materials. In response to the above problems, Lin[10] proposed to strictly control the material quality of construction projects from the following four aspects: To enhance building materials cost management, several critical steps should be taken. Firstly, it is essential to focus on input supervision of materials by ensuring rigorous oversight of material procurement to guarantee that the quality meets the required standards. Secondly, emphasis should be placed on material storage supervision, including regular inventory checks to maintain proper material conservation practices. Thirdly, improving the professional competence of material inspection personnel is crucial; this involves actively nurturing high-quality inspection and warehouse staff. Lastly, effective on-site construction supervision is vital to prevent substandard work and ensure consistent material quality during the construction process. Ma[11] suggested that the new building materials industry has problems such as low concentration, backward technology research and development, and a single mode of investment and financing. She recommended that construction enterprises should intensify supervision and promotion of new building materials and give them more attention. Additionally, it was suggested that these enterprises should restructure the industrial composition of new building materials, decrease actual production energy consumption, enhance independent innovation capabilities, aim to acquire core technology in low-carbon new materials research and development, and propel market-oriented material development.

Işıkdag et al.[12] estimated the construction material prices by using Autoregressive Integrated Moving Average and Nonlinear Autoregressive Neural Network, respectively. The above models significantly improved the predictability of construction material costs and effectively avoided cost overruns. Vedartham et al.[13] compared the cost of traditional building materials and green building materials through quantitative investigation, and found that the replacement of conventional building materials by sustainable building materials could reduce the building cost by 3.15%. Giesekam et al.[14] examined the economic, technical, practical and cultural barriers to the adoption of green and low-carbon building materials through a survey of construction professionals and interviews with industry leaders. They highlighted the high cost of building materials, unclear managerial responsibilities, industry culture, and the absence of carbon emission standards for products and buildings as key obstacles hindering the adoption of low-carbon building materials. In response, they proposed several solutions: firstly, involving professionals early in the supply chain management process; secondly, utilizing life cycle costing effectively for material cost calculations; thirdly, establishing and enhancing material cost management mechanisms; and fourthly, revising contracts and tender documents. In conclusion, within the low-carbon economy framework, managing the cost of new green building materials poses a challenge for Chinese construction enterprises, yet it is a crucial step towards achieving the objectives of “carbon peak and carbon neutrality”.

Previous research indicates that the ongoing growth of a low-carbon economy will encourage the emergence of a new market for green construction materials. New green building materials have the potential to lower construction projects’ overall costs. However, the cost of new green building materials is difficult to control due to three factors: first, the new building materials did not perform well in the procurement, warehousing, and construction environments; second, the price of new green building materials is high; and third, there are differences in industry standards. However, the view of material cost control is limited to a certain point of view, such as procurement management, inventory management, and construction management. There is no systematic study of the formation process of material costs, and there are few studies on the enterprise’s management mode and the responsibility norms of enterprise managers.

This paper primarily addresses the aforementioned issues by examining new green building material research and development, material market price fluctuations, material cost management investments, environmental accounting, and employees’ economic awareness. It provides relevant suggestions and countermeasures to tackle the challenges in cost management of new green building materials and achieve the effective integration of cost management and control in this sector.

2. Significance and Influence of Cost Management of Building Materials in the Context of Low-Carbon Economy

Low-carbon economy is an innovative approach to technology, industry, and institutions, based on sustainable concepts, which aims to minimize the waste of energy and resources, reduce greenhouse gas emissions into the air, and achieve dual economic benefits for society and the environment[15]. Cost management refers to the method of scientific management of various expenses in enterprise operations[16]. It focuses not only on post-analysis, but also on pre-planning and in-process control. Cost management encompasses activities such as cost target setting, cost budgeting, cost control, cost analysis, cost-benefit evaluation, performance assessment, and continuous improvement. It is a management method that takes the whole enterprise as the management object and implements it according to the future development trend of the enterprise. The construction sector serves as a key industry propelling China’s economic advancement[17].

In addition, the cost management of building materials under the low-carbon economy should follow the principle of circular economy[18]. Reduction, reuse, and recycling are the cornerstones of the circular economy. Reduction refers to the material resources used in production and consumption activities, and it advocates for a decrease in resource input and pollutant discharge during the early stages of economic activity in order to ensure the normal progression of production activities. In order to ensure the quality of service, reuse refers to extending the use of resources and the service cycle as far as possible. Packaging containers or products made from resources can be reused multiple times in their original state, preventing resource products from ending up in the trash too soon and effectively preventing the phenomenon of excessive use of one-time resources. Reusing materials after they have served their intended purpose is known as recycling. From the standpoint of the circular economy, the cost of building materials is integrated into low-carbon green buildings. This means that consideration must be given to the application of environmentally friendly and energy-efficient building materials, as well as the creation of environmentally friendly and energy-efficient building use plans that take into account the structural and functional characteristics of individual buildings.

Keep construction input costs under strict control during the design phase[19], avoid using expensive building materials; carefully analyze building performance and capital investment to use energy-efficient and environmentally friendly materials rationally and raise the overall ecological and environmental protection level of building projects. It is possible to choose reasonable thermal or sound insulation materials in accordance with the building’s intended use. It is evident that in order to achieve a healthy and sustainable development of construction activities, a circular economy necessitates the systematic avoidance of waste in building material resources and waste discharge in economic activities.

To ensure that construction enterprises have adequate liquidity, continuous investment is necessary at various stages. However, these investments face various uncertainties, such as market demand fluctuations, policy changes, and project alterations[20]. By strategically allocating funds and proactively mitigating financial risks, enterprises can maintain liquidity across varying economic cycles and market conditions to fulfill diverse payment obligations. It is imperative for businesses to swiftly respond to emerging risks and maintain adequate reserves to address unforeseen contingencies, thereby minimizing the financial impact of unexpected events.

2.1 Optimize fund allocation

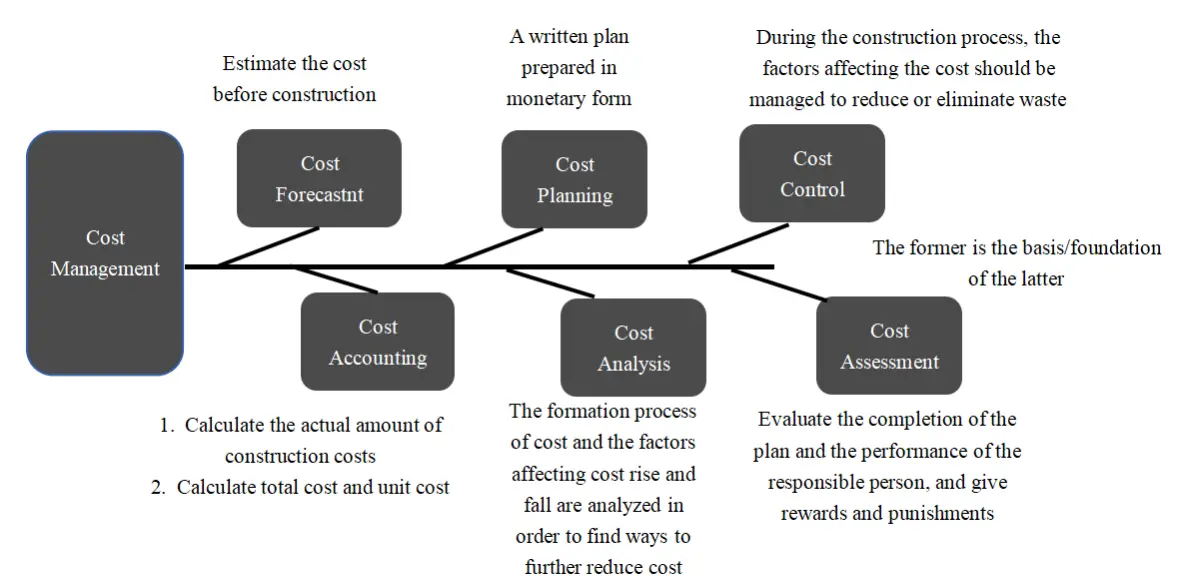

China is currently investing more money in a wider range of construction projects, including green building projects. However, closing the construction financing gap is still difficult. The primary cause of this problem is the lack of a flexible and all-encompassing strategy for managing the cost of building materials. The cost of new green building materials fluctuates during the implementation of low-carbon building projects, making it difficult for traditional cost control methods to track and dynamically manage these expenses[21,22]. This can lead to a reduction in cost control efficiency and possibly even halt construction progress. Therefore, by carefully planning for material work at the beginning of the project and optimizing cost management strategic for new green building materials, construction companies can improve cost management (Figure 3). The choice of building materials must be practical in addition to fulfilling the requirements of the building purpose. The management team of the company should estimate the cost of the building materials prior to starting the construction project and create a budget based on the findings of the calculations. The cost strategy must adhere to the fundamental ideas of the circular economy[24]. The elements influencing the cost should be controlled and monitored during the building process, and under certain conditions, appropriate action should be made to minimize or completely eradicate waste and loss. In order to find even more ways to cut costs, the second step is to compute the real construction costs and evaluate the elements that determine cost growth and decline as well as the creation process of costs. Ultimately, incentives and sanctions for management personnel’s cost assessment will be determined by how well cost management and control are executed[23].

These approaches can efficiently regulate the procurement of building materials across all construction activities, facilitating the optimal allocation of enterprise funds.

2.2 Prevent financial risks

The procurement, transportation and construction stages of new green building materials have high risks[25,26]. The risks mentioned stem from multifaceted factors including market price volatility, erratic transportation expenses, and insufficient hydrological and geological assessments of construction sites, all of which can impede construction timelines, escalate project costs, and introduce financial uncertainties. In order to ensure the orderly development of construction projects, it is necessary to carry out comprehensive budget management for new green building materials during construction[27]. Construction firms can enhance the management of building material costs by implementing stringent budget controls, thereby ensuring expenses are maintained within manageable limits. This proactive approach serves to mitigate financial risks, safeguard the profit margins of the company or project, and uphold overall financial stability.

2.3 Fluctuations in the price of building materials

Growing numbers of building projects are implementing the “four savings and one environmental protection” principles land conservation, energy efficiency, water conservation, material conservation, and environmentally friendly building materials-as the low-carbon economy has gained traction in recent years. As a result, variations in material pricing and manufacturing costs are being driven by the growing market demand for new green building materials[28]. Similarly, the rise in raw material prices, energy prices,Industry policy and labor costs will also lead to rising prices of building material[29].

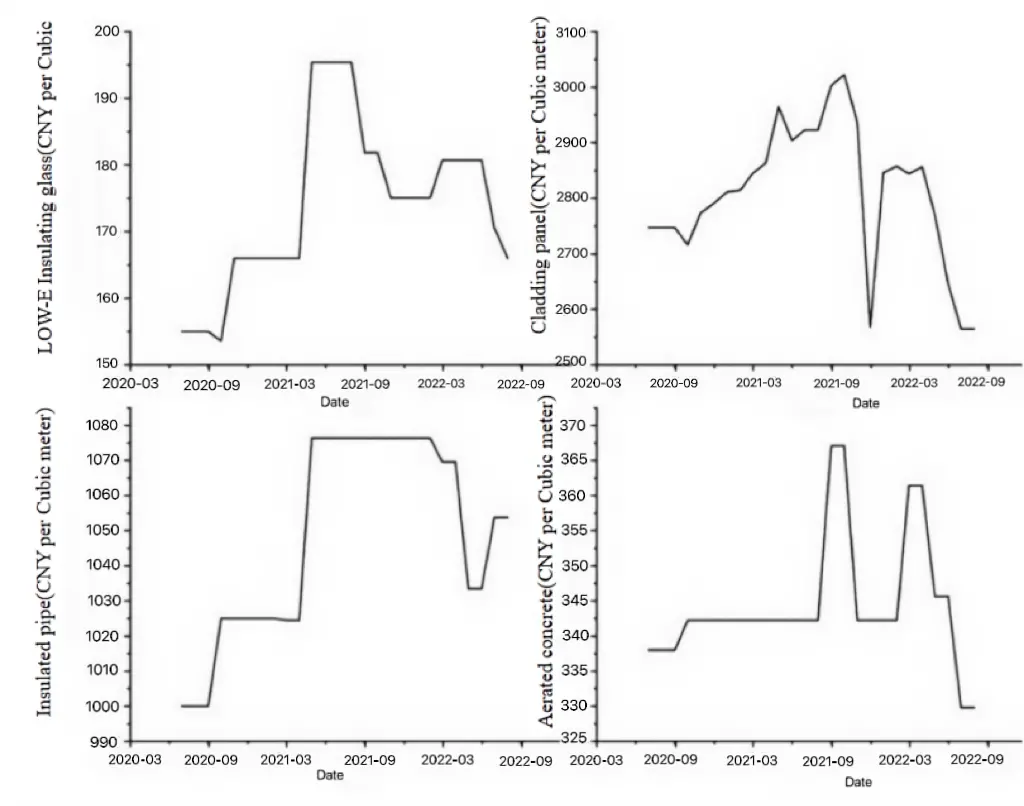

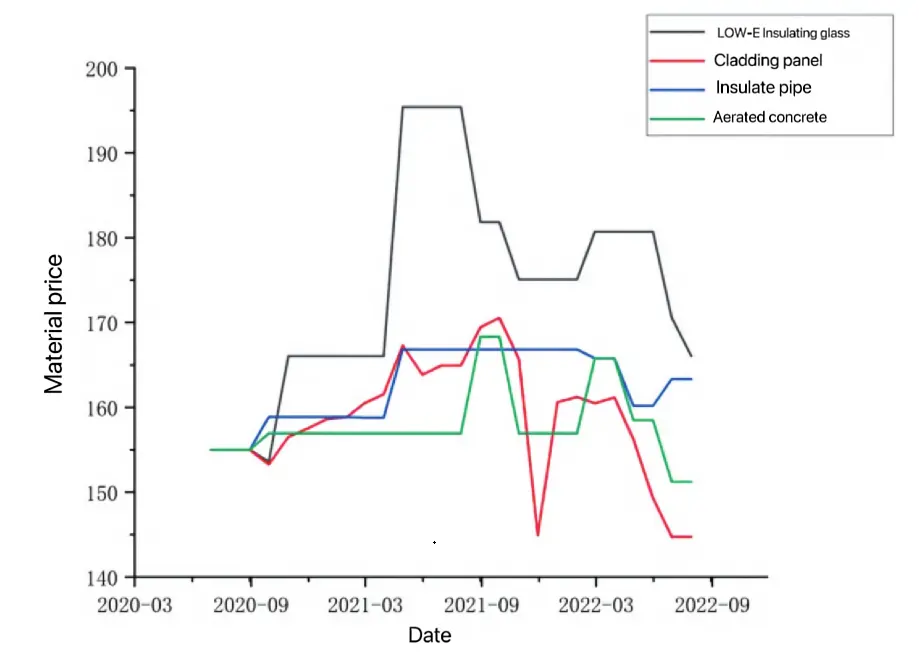

The primary cause of price volatility, industry policy, has a bigger influence on market dynamics. The price trajectory of a few energy-saving items in Hengyang City, is depicted in the following figure, which uses information on the city’s information prices from March 2020 to September 2022 as a data source. Figure 3 illustrates that the price fluctuation of energy-saving materials is irregular, with a different fluctuation amplitude than that of ordinary materials. A method of processing all the data at the same beginning point was used in order to ascertain that the four energy-saving materials in Figure 3 have the same fluctuation trend (Figure 4). As can be seen from Figure 4, the price increase points of the four energy-saving materials are the same; that is, the price was stable before October 2020, which may be caused by the local construction industry not using a lot of energy-saving materials at that time, resulting in oversupply. After that, Hengyang City forwarded the Notice of the Hunan Provincial Department of Housing and Urban-Rural Development on Strengthening the management of civil Buildings Energy Conservation, and green buildings in our Province. At the same time, with the promulgation of a publicity system for building energy-saving products (materials), the relationship between supply and demand of energy-saving materials has changed, resulting in fluctuations in line with market rules.

Figure 4. Hengyang City part of the price of energy-saving materials. (Data source: https://www.gldjc.com/). CNY: Chinese Yuan.

Fluctuations in building material costs invariably result in heightened construction expenses, thereby impacting both the construction timeline and project quality. With rising material prices, construction firms face increased expenditure[30]. In response to the above, many construction units will choose to delay the purchase of materials and try to purchase them after the price drops. If construction companies use low-priced building materials or cut corners to reduce costs, the quality of construction projects will be difficult to guarantee, leading to quality problems and rework, which will invisibly increase project costs and then harm the construction industry[31].

2.4 Increase the difficulty of cost control

In the past,the management of construction projects in China primarily focuses on the linear management mode of superiors and subordinates[32]. This kind of management mode has poor flexibility, and the supervision effect is not obvious, which will make the management procedure of building materials relatively complicated. At present, the material enterprises mainly use BIM technology[33] is mainly used to try to track and locate material information and solve the problems existing in construction logistics management. At the same time,by monitoring green building materials, BIM technology recycles and processes green building materials that have reached their useful life to avoid material waste and pollution. In addition, innovative green building materials produced in the material market can be actively tracked, and replacement building materials can be reasonably selected to further improve building performance based on the original[34]. However, due to the high cost of software development and the use of BIM technology[35], relevant technical personnel are required not only to have solid basic knowledge but also to have rich work experience, as well as strong innovation ability and programming ability. Additionally, there is no way to complete the work in the short term for the creation of the cost database and software development; these tasks require a lengthy procedure. The procedure requires a significant investment of both material and labor resources because software upgrades and maintenance are quite expensive. As a result, creating a full software system requires a large financial investment. However, the database still requires significant expenditures for upkeep and use, and smaller businesses find it difficult to pay for these kinds of charges, making cost control almost impossible.

On the other hand, most of China’s current green building materials[36], energy saving and emission reduction equipment are imported from abroad, with a high degree of international dependence and difficult to control material costs. At the same time, due to technological limitations, inevitably, the construction quality is not ideal, and the above factors further increase the uncertainty of cost control.

2.5 Expand investment in management costs

To address the mounting challenges posed by the new green building materials market within the low-carbon economy, enterprises must ramp up their investment in management costs. Firstly, neglecting resource allocation in cost management and overlooking supply chain management[37] can give rise to numerous issues. For instance, inadequate planning of material quantities in construction projects can lead to production delays, material losses during construction, and material deformities during transportation[38]. Such oversights may result in excessive material procurement, leading to resource idleness or wastage, ultimately in[39] flating construction costs. Additionally, there may exist information asymmetry between the upstream and downstream segments of the construction materials market[40]. In the construction sector, enterprises operate on a large scale with intricate supply chains, leading to the dissemination of information and potential amplification of system errors throughout the supply chain. The continuous magnification of errors can result in information distortion and uncertainty[41]. Moreover, downstream customer preferences’ variability can cause erratic purchasing patterns, while uncertainty stemming from inaccurate market forecasts by upstream suppliers can further complicate supply chain management. Furthermore, the rapid evolution of the construction industry has rendered traditional building materials inadequate to meet enterprise development requirements, particularly in achieving low-carbon energy-saving objectives[42]. Consequently, there is a pressing need to leverage intelligent information technology and new energy sources in the Internet era to upgrade and transform building materials. The emergence and advancement of China’s next-generation information and communication technologies are driving the transformation of the construction engineering industry, notably through technologies like the Internet of Things[43], cloud computing and information physical systems[44], big data[45] and deep learning[46]. Concretely, China is currently utilizing 3D printing technology in the field of building materials (Figure 5), such as contour technology[47], D-Shape[48], and printing concrete[49]. In the future, the functions of China’s 3D printers will be more diversified, and they will inevitably play a greater role in realizing the industrialization and intelligence of the construction industry. For example, installing print nozzles to print concrete, installing mechanical arms for wall construction and installing glue droplet heads for sand bonding printing[50]. At the same time, China will also transform and utilize building materials through new energy technologies. For example, forced-ventilation active walls, green or ecological active walls, and other efficient improvements will address the current high carbon emissions issues in energy saving in buildings[51].

Figure 5. Prices fluctuate after four materials are selected from the same starting point. (Data source: https://www.gldjc.com/).

In light of this, it is crucial for the Chinese enterprises to proactively acknowledge that the adoption of intelligent information technology and new energy sources will inevitably raise management costs[52]. Consequently, construction enterprises should enhance their investment in management costs. With the increased investment in enterprise management costs attributed to the upgrade and transformation of building materials through information technology and new energy, project engineering personnel can leverage network information systems to achieve dynamic material management[53]. This approach can enhance material management efficiency and quality, ultimately facilitating the advancement of construction projects.

3. Issues in Cost Management of Building Materials in the Context of Low-Carbon Economy

3.1 Inadequate cost management system

At present, the inadequate cost management system of some construction enterprises has led to the inability of cost management to exert its due value[54]. Certain construction companies oversee the management of construction projects, but they fail to disclose in the cost management system the preparatory and coordinating work involved in the construction process. Moreover, the material procurement cost management in many construction enterprises still relies heavily on an extensive management approach, lacking comprehensive and efficient procurement management methods and technological applications[55]. The lack of precision in material planning during the construction phase often leads to material shortages or surpluses, thereby increasing material procurement costs for the enterprise[38].

Enterprises’ ability to implement cost management effectively is impacted by their lack of a strong cost control model and procedures. Thus, the primary cause of the inadequate cost control effect is the flawed cost management system.

3.2 Incomplete building material management system

New green building materials are being used in an increasing number of Chinese construction projects these days. However, the phenomenon of waste arises from inadequate supervision of material application, scientific management of new green building materials, and ineffective management of the procurement, utilization, and recycling processes of materials[56]. These difficulties create a mismatch between the purchased materials and the project requirements, which significantly raises the cost of the materials and ultimately lowers the quality of the entire project. They also make it difficult to effectively control the total cost of construction[57]. At the same time, the company’s management personnel in the implementation of the link due to cost management awareness is weak, the management of arbitrary and sloppy[58], which brings greater difficulties to the management of construction materials, and the problems existing in material management are difficult to effectively solve. In the long run, these challenges can result in significant overspending on material costs, substantially diminishing project profitability and potentially resulting in financial losses. The deficient construction materials management system significantly inflates the total cost of construction projects, undermining the enhancement of economic efficiency for enterprises.

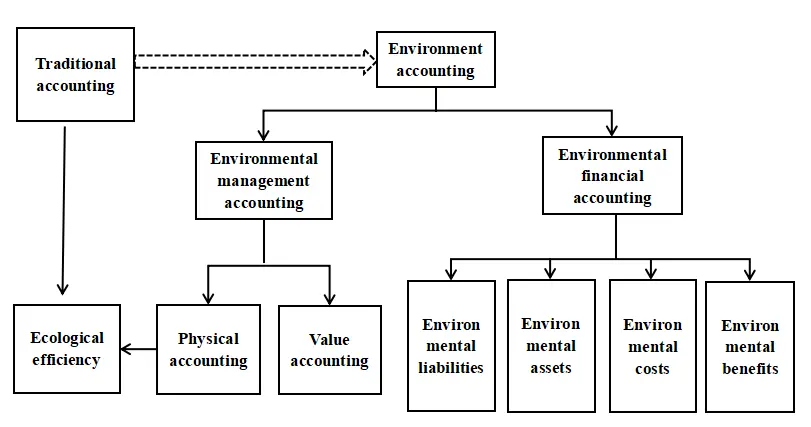

3.3 Unstandardized environmental accounting in enterprises

The research on environmental accounting in China began in the 1990s, relatively late compared with developed countries[59]. There is a notable opportunity for ongoing enhancement in the disclosure of environmental accounting information by enterprises, with relevant authorities often overlooking this aspect. However, the adequacy of environmental accounting information disclosure significantly influences enterprise cost management and environmental protection efforts.

Following the introduction of the “carbon peak and carbon neutrality” objective, enterprises have been proactively engaging in self-assessment and corrective measures. In the construction sector, recognized as one of the most polluting industries, the incorporation of environmental costs into accounting practices holds particular significance. Some enterprises are unwilling to publicly disclose their actual situation and relevant data[60], which makes it difficult for the outside world to assess the environmental risks and inputs[61] of enterprises. The above phenomenon indicates that some enterprises in China have not realized the importance of environmental accounting information disclosure, and have ignored the impact of environmental accounting information disclosure on enterprise performance[62,63]. Meanwhile, the construction industry still lacks a unified standard for environmental accounting information disclosure[64]. Simultaneously, the construction industry faces a dearth of standardized guidelines for the disclosure of environmental accounting information. The absence of uniformity makes it challenging to compare environmental inputs across enterprises, given the varying scopes, methods, and volumes of inputs within each construction firm[65]. Consequently, this disparity results in a lack of standardized information disclosure formats in the industry.

3.4 Low economic awareness among employees

Material costs represent a significant component of the direct costs associated with green building projects. However, the management of material costs is often overlooked due to the limited economic awareness among employees across different departments within companies. For example, the construction personnel only pay attention to the output and quality of the project[66], to complete the project within the scheduled period, the construction of various construction machinery and equipment is unreasonable. The addition of construction personnel at will resulted in the construction of numerous materials, some of which were stolen from time to time. Project designers only pay attention to the aesthetics and practicability of buildings and do not consider the amount and cost of building materials in the design process[67], which leads to high costs in subsequent construction. Furthermore, there are disparities in the professional caliber of materials management staff, certain workers lack contemporary scientific expertise and managerial abilities, and there is inadequate execution and oversight of diverse materials systems.

The above factors lead to the lack of rationality and scientific structure of the supply chain of construction engineering projects[68], which makes it difficult to effectively control the overall economic cost of the project.

4. Countermeasures and Suggestions

4.1 Develop new materials suitable for economic development

China’s construction industry is transitioning to green buildings against the backdrop of a low-carbon economy, and the use of green building materials has expanded dramatically. To encourage the modification of the industrial structure, green, low-carbon building material companies should create and manufacture green building materials. Through the research of ecological environmental materials, the research and development of materials combined with environmental protection functions, such as carbon fiber materials[69], renewable materials[70] and composite phase transition materials[71] (Figure 6). The specific measures are taken as follows.

4.1.1 Production of green building materials using renewable energy

By adopting renewable energy, the production process can reduce the dependence on scarce fossil fuels and replace them with endless renewable resources, thus reducing the environmental burden[74], which makes the manufacturing process of green building materials more environmentally friendly.

For example, through the production of green building materials using solar energy[75]. The solar energy can be developed and utilized in two forms: passive and active. In order to gather solar energy, passive solar energy thermal conversion is used. Then, in the building, solar heat is supplied to the user through heat exchange[76]. The solar heating house system[77] collects the heat generated by solar energy and converts it into heat energy to heat the house by setting up heat-collecting components. The installation location of heat-collecting components is usually the window and wall surfaces of the building. Because the wall is the largest component in the building, its application is mainly concentrated on the development of a heat storage wall, which has the greatest impact on heat collection. A method of heating a house through a broad area of balanced radiation heat dissipation is a solar low-temperature hot water floor[78]. The house has a special solar collector installed outside, and once the collection gathers heat, low-temperature water diffuses the heat into the building. Due to its more balanced heating that offers users hot water supply, home heating, and other services, this heating technology is widely employed throughout the world[79]. The active application method is mainly used by converting solar energy into electric energy, and the photovoltaic power generation device arranged on the roof, wall, and window sill is used to convert light energy to electric energy. By combining photoelectric conversion materials[80] and building materials[81] to create structures with both architectural beauty and photoelectric conversion functionality. For instance, photoelectric glass[82] can be used in some structures in place of conventional glass and simultaneously generate power. This cutting-edge building element will unavoidably influence the future advancement of building materials and offer additional resources for the growth of the construction sector.

The wide application of solar photovoltaic technology[74] has made the manufacturing process of green building materials more environmentally friendly. Similarly, wind energy, as a renewable energy source, can provide green electricity for the production of building materials through wind power systems[83], reduce the dependence on traditional electricity sources.

4.1.2 Improve the processes of innovative green building material development and manufacture

Through the exploration and innovation of new raw materials, such as biodegradable plastics and bio-based materials[84], can significantly reduce the dependence on limited resources and reduce carbon emissions in the production process.

According to the source of raw materials, degradable materials can be divided into three categories: natural type, natural improved type, and chemical synthesis. Different types of degradable materials have different characteristics and application ranges. Degradable materials fall into three groups based on the source of their basic ingredients: natural type, natural enhanced type, and chemical synthesis. Degradable materials come in a variety of forms with varying properties and uses. A novel form of interior wall material for construction, silica-calcium straw light body wallboard[85] uses crop straw, tail leftovers, and other natural material waste to create wall materials that can be used for construction. Crop straw, bonding materials, and supplementary materials for reinforcing materials are its primary raw resources. Through a certain process, using the characteristics of physical and chemical reactions between materials, they can be naturally released after solidification and applied to the building interior wall. The material has the advantages of good seismic and compressive performance, fire and moisture resistance, no toxicity to the environment as a whole, a good sound insulation effect, and will not discharge hazardous waste to the environment in the production process. At present, this material has become a new type of environmental protection material, widely used in the interior walls of buildings.

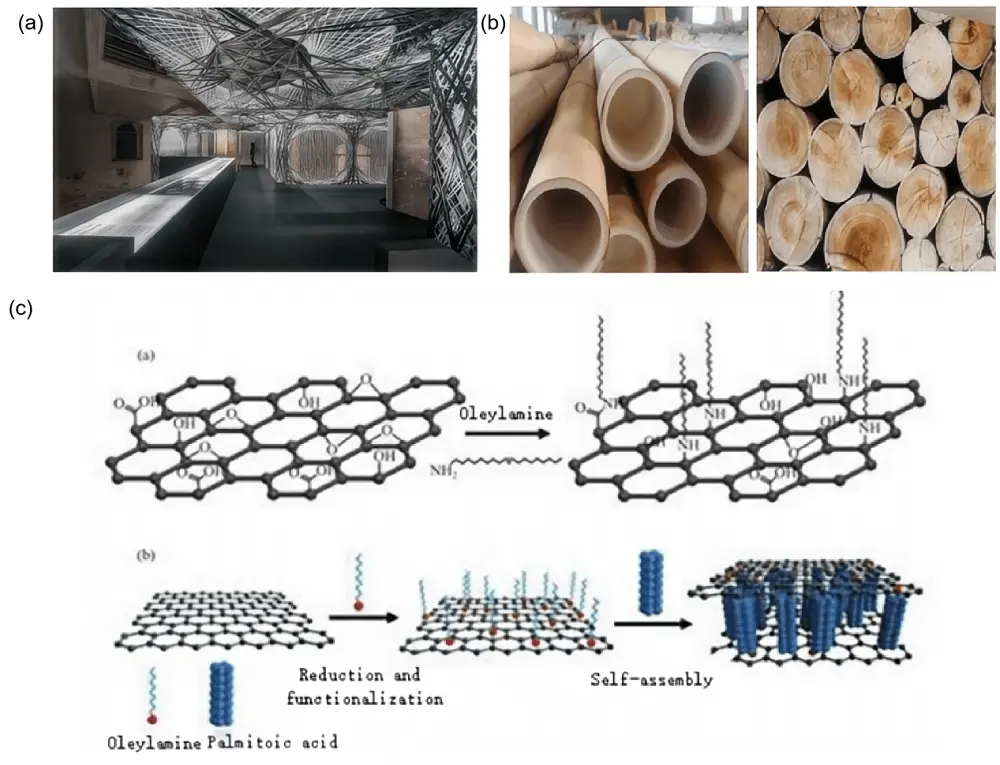

Bamboo has long been used as a building material in China’s construction sector. Bamboo is a renewable, easily grown, and multipurpose material that is also kind to the environment. In addition, it has excellent tensile resistance, minimal shrinkage, high toughness, and high strength. As a result, the use of bamboo for contemporary windows, doors, walls, and other construction materials has grown in importance and has been researched in the field of architecture[86].

At the same time, the improvement of the production process is also an important means to achieve sustainable building materials. Using advanced manufacturing techniques such as 3D printing and nanotechnology[87], not only improves the performance and quality of materials but also helps to reduce energy consumption and waste generation in the production process.

Cement-based materials, as the main 3D printing building materials[88] are 3D printed based on the principles of rheology and cement hydration[89-91]. Its research and development[92-94] includes adding different ratios of admixtures to control the rheology and shrinkage of cement-based materials, increasing the strength, toughness, and durability of cement-based materials, and improving the interlayer bonding performance of printing materials. By choosing different aggregates, the weight of the structure is reduced[95]. In the management of the development of printing materials, performance evaluation methods. At present, 3D printing technology has been realized in the field of building materials: 3D printing concrete[96], 3D printing aluminum alloy[97], and 3D printing slag base polymer material[98].

Nanotechnology primarily pertains to the investigation of the interactions and principles of motion among atoms, molecules, and electrons in the material composition system, operating within the 0.1-100 nm scale range. The ultimate goal of nanotechnology is to enable human control over atoms and molecules, leading to the development of products that fulfill specific human needs. These days, nanotechnology is extensively employed in novel construction materials including nano-coating and nano-cement coatings[99] which are typically applied to buildings’ exterior and interior walls for painting. Conventional coatings typically exhibit flaws including inadequate finishing and unstable suspension, however novel nanocomposite coatings[100] incorporate nanoparticles and additional technologies to attain resistance against aging and radiation. In the building sector, it has demonstrated its distinct appeal. The functional transformation of materials benefits from the application of nanoparticles. The preparation of external wall coatings using nanomaterial-modified nano-organic and inorganic composite emulsions[101] and nano-silica series colloids[102] can enhance the coatings’ outdoor water resistance, scrub resistance, and suspension stability[103]. Ordinary cement concrete is prone to cracking and destruction during usage because of its high stiffness, low flexibility, and several intrinsic faults.Nano-concrete’s development[104] has successfully resolved this issue. When compared to regular concrete, nano concrete has been used in a wide range of fields and industries, significantly enhancing the quality of construction projects and improving people’s lives and productivity.

4.1.3 Develop recyclable and recycled new green building materials

As the economy and society continue to advance, and waste management systems improve, the concept of establishing “waste-free cities” has emerged as a strategic goal for numerous countries and cities. Consequently, the recycling and reuse of materials serve as a pivotal focus in the production of green building materials and represent a crucial strategy for advancing the development of “waste-free cities” and “waste-free factories”. This idea advocates the recycling and recycling of as many resources as possible during the life cycle of building materials[105], to reduce the over-dependence on limited resources and to minimize the rate of resource depletion. In practice, the recycling of materials includes the recycling of waste building materials[106] and the reprocessing and remanufacturing of discarded products and components[107]. For example, the waste concrete can be broken into recycled aggregate[108] by recycling the concrete[109], and then used for new concrete products. Using waste concrete to produce recycled aggregate concrete[110], can save 62% of limestone resources and reduce CO2 emissions by 20%[111].The recycling of waste concrete can protect and balance the natural resources and living environment for a long time. In the process of waste concrete treatment, “reduction, recycling, reuse” is the basic principle. As a renewable resource, recycled concrete reacts during construction and is transformed into new “green building products” in different ways. This recycling method not only reduces the demand for new raw materials but also reduces the generation of waste and the negative impact on the environment.

4.2 Innovation in the technical department of the building materials industry

The research and development of new green building materials heavily relies on the backing of science and technology, and China is continuously bolstering its efforts in this domain. Currently, China has attained proficiency in several research and development technologies related to building materials. For example: 3D printing technology, photovoltaic energy technology, and recycled building materials backfill construction technology[112]. Hence, construction enterprises should establish innovative research, development institutions and systems, and enhance the construction of leading organizations for new materials[113]. Specific measures to achieve this include:

1) Creation of administrative departments for the new materials industry by management departments at all levels[4], with the main responsibility being the supervision of research and development for new materials and the creation of comprehensive implementation plans.

2) Establishing a “new green building materials service platform” to collect data on prices, market demand, and the range of new green building materials. Additionally, to enable cooperation with pertinent building materials companies in order to maximize resource allocation[114].

3) Improvement of policies and standards by the government to establish a sustainable development mechanism for materials research and development[115]. The construction of new materials plays a vital role in the modern high-tech industry, requiring rapid advancement through technological innovation and capital investment. Additionally, the government should guide and support the rational development and application of new materials by enacting relevant laws and regulations, offering financial assistance, and ensuring enterprises adhere to market-oriented principles and international standards in their development endeavors.

4.3 Optimize the cost management system

A well-structured construction material cost management system is crucial for efficiently managing economic costs. It is imperative for relevant management personnel in enterprises to address the existing challenges in construction economic cost management by prioritizing the enhancement of the construction material management system. Specific measures to achieve this include.

4.3.1 Improve the cost accounting system

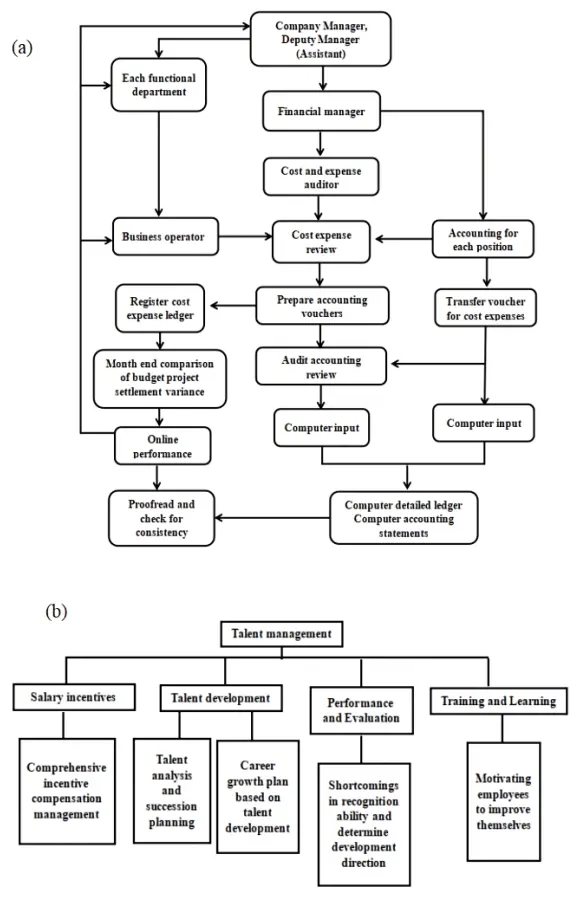

To align with the market economy and the development objectives of construction enterprises, it is essential for construction enterprises to establish a rigorous cost management system and talent management mechanism[116] (Figure 7) to enhance the refinement of the cost management system. Simultaneously, the construction budget management system should be enhanced by developing suitable cost assessment standards for each department and refining cost targets to eliminate ambiguity in roles and responsibilities. Improving the cost accounting system[117] will help clarify the workflow and details of cost management, enabling the enforcement of responsibilities and duties of cost management personnel.

4.3.2 Improve the financial and accounting supervision system

According to the policy changes and their own development needs, enterprises regularly sort out and improve the various systems and processes, and supervise the finance and accounting[119] integrated into the whole life cycle of the project and serve the purpose of internal control and management of enterprises. Improving the governance process for decision-making. For example, is essential to guaranteeing that procedures for accounting scrutiny are successfully involved in important economic decisions. By combining accounting oversight with internal control mechanisms, evaluating internal controls on a regular basis, spotting problems with internal control mechanism design and operation, and encouraging the improvement of enterprise internal control management, internal control efficiency can be consistently evaluated[120]. Enhancing the internal control system is also necessary to protect the independence and legitimacy of accounting supervision.

4.4 Improve the material cost control system

The procurement, transportation, and storage stages of construction materials are interconnected. Hence, companies must enhance material cost control across these stages and upgrade the material cost control system.

4.4.1 Procurement phase

Material cost control during the procurement stage primarily involves managing the quantity and unit price of materials purchased. Upon issuing the approved material demand plan, tasks are allocated based on major categories or specific materials, with planners developing the material procurement plan considering factors like material demand timing, available inventory, reserve demand, safety stock, among others. Once the procurement plan is finalized, the purchase quantities are aggregated by major category and time phase[121]. Subsequently, buyers initiate inquiries based on the material categories outlined in the procurement plan, focusing not only on price but also on material quality, delivery lead times, and post-sales services to minimize quality costs and ensure timely deliveries. Following the determination of purchase quantities and unit prices, the purchase costs are computed. If the calculated cost exceeds the target cost, further controls are implemented on quantity and unit prices until the calculation aligns with target cost management requirements, enabling the issuance of the purchase plan[122].

4.4.2 Transportation stage

The enterprise’s current transportation resources, which possess the qualities of informatization, coordination, and unification, serve as the foundation for the creation of the ideal transportation management system[122]. The management of transportation distance, vehicle types, transportation routes, and completed product component protection should all be included in the building material transportation management system. Since the distance between businesses and the location where building supplies are procured directly affects transportation costs, the lowest transport distance should be selected first[123]. Additionally, in order to choose vehicles that match well and improve loading efficiency, it is crucial to take the shape and size of the components into account when choosing transport vehicles. Additionally, it is essential to evaluate the state of the roads before deciding on a transportation route in order to prevent potential damage from potholes or uneven surfaces, which could result in higher expenditures because of material damage, collisions, or deformations. The preservation of raw materials and completed goods during transit must be given first priority. Construction delays and increased time-related expenses might be caused by improper material handling and inadequate protection. To avoid damage during shipment and lifting of components and accessories, pre-transport packing utilizing materials like plastic foam and sponge as well as putting policies in place such support fixation and secure binding are advised.

4.4.3 Warehousing stage

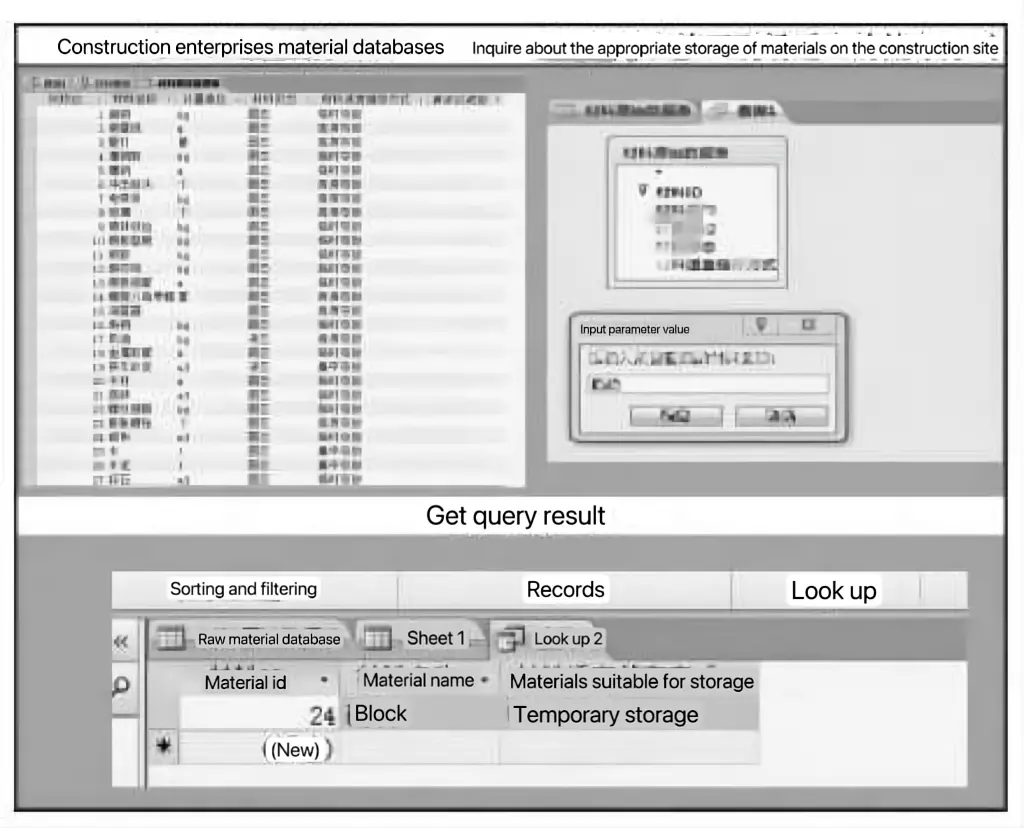

Once the materials arrive at the company’s warehouse, the purchaser should inform the inspection department to conduct a thorough material inspection in accordance with the procurement contract. The purchaser, along with the warehouse keeper and quality inspector, should participate in the arrival inspection process[124]. The storage department should be informed and storage procedures should be started in order to get ready for material placement if the inspection results meet the necessary standards. It is easier to create an inventory ledger for each item if materials are stored according to the project number. If materials don’t pass the examination, they should be sent back or, with the client’s consent, degraded for usage. Businesses can create a Building Information Modeling materials database (Figure 8) and digitally record all materials on the computer system to stop building materials from being lost or damaged[126]. Simultaneously, counting the number of supplies allows the warehouse manager and buyers to plan for the cost of the next purchase.

4.5 Improve the material management system

Establishing a well-defined management system is essential to ensure that the responsibilities of personnel involved in building materials management are effectively implemented. By standardizing the responsibilities of staff members through systematic constraints, the management system helps clearly define and allocate responsibilities.

4.5.1 Whole-process supervision of materials

In order to supervise on-site material management in accordance with regulations, the business must designate specific materials management personnel[127]. To make maintenance and access easier, materials should be kept in their proper places and arranged. The allocation of materials for each project stage and work area should be part of a comprehensive plan for material utilization at the site. In order to enhance project efficiency, it is imperative to reduce the likelihood of material loss and decrease on-site stacking.

4.5.2 Strengthen the inventory management of materials

For items to be properly followed from purchase to storage, a strict registration and inspection system is necessary. To ensure correct cost accounting for engineering materials in the future, materials from different projects should not be mixed together and should instead be registered separately[128], The management of the business must place a high priority on the inventory of returned goods and order the management department to create a special system for handling returned goods, delegating accountability to each project manager. Materials must be returned to the warehouse after the job is finished, and thorough return documentation must be kept[124].

4.5.3 Establish the material cost assessment system

Enterprises should actively apply the material cost assessment mechanism to better manage and use materials[129]. Monitoring how building materials are used throughout departments like purchasing, construction, and warehousing can help businesses become more efficient and cost-effective. Preventing problems such as material waste, differences between received amounts and lists, and neglecting to return extra items to the warehouse following project modifications are vital. Companies can streamline their material management procedures and cut down on wasteful spending by carrying out prompt investigations and putting in place efficient control measures[130]. To encourage each participant, prizes and penalties will be assigned based on the relevant requirements of the material cost objective, actual indicators, and the plan and forecast.

4.6 Establish a material price risk management mechanism

4.6.1 Establish the material risk management mechanism

Construction companies should set up a system for managing material risk, keep an eye on and assess the effects of changes in the cost of new green building materials, promptly modify their production and business plans, and lower risks[131]. Businesses can mitigate the risks associated with new green building material price changes by fortifying their supply chains, maintaining building material stockpiles, and routinely revising their purchasing strategies[68]. To guarantee the precision and thoroughness of price fluctuation management of new green building materials, relevant staff should promptly gather, analyze, and classify market information of building materials and become proficient in more information sources through more channels.

4.6.2 Fully grasp the material price fluctuations

Making well-informed procurement decisions requires analyzing the state of the market for new green building materials as well as the pricing trends of construction supplies. Through comprehensive analysis, organizations can anticipate and evaluate possible price fluctuations for materials[132], offering crucial information for material sourcing plans. Furthermore, it is important to intensify market research endeavors and establish dynamic management strategies congruent with construction material costs. To remain aware and responsive to market variations, it is imperative to designate specialized staff to oversee market dynamics, follow real-time pricing changes, and guarantee the sufficiency and timeliness of market surveys. By taking a proactive stance, businesses can efficiently manage their procurement processes and respond quickly to shifting market conditions[133].

Relevant personnel can gather and integrate the detailed material price information via the Internet, e-commerce platforms, and other channels during the market investigation and analysis process of new green building materials. This will enable them to quickly and accurately ascertain the material market’s pricing information[134]. Based on this, it forecasts changes in building material prices in the future, understands the fundamentals of the building material industry, and offers businesses a useful resource for developing innovative solutions and preventative actions.

4.7 Standardize the environmental accounting of enterprises

From a governmental standpoint, encouraging regulations and transparency should be implemented by relevant authorities to encourage construction companies to provide environmental accounting information (Figure 9). The building industry can adopt sustainable practices and improve market supervision if the government supports openness and transparency in environmental accounting information[135]. To support these efforts, it is also crucial to actively improve the laws and policies governing the disclosure of environmental accounting information and to make theoretical research investments. In addition to guaranteeing adherence to legal requirements, strengthening the framework for environmental accounting information disclosure promotes an accountable and conscientious environmental stewardship culture in construction companies[136]. This proactive strategy has the potential to improve industry-wide sustainability policies, raise environmental awareness, and oversee markets more effectively.

Starting from the long-term interests of construction enterprises and the society, enterprises should actively disclose environmental accounting information[137]. This can be disclosed from the aspects of environmental costs, material governance and management costs, environmental investment, and the company’s environmental protection responsibilities. In addition, the disclosure form of environmental accounting information can not only be reflected in the form of notes to financial statements[138], and it can also be shown with complete accounting reports and social responsibility reports, making the disclosure of environmental accounting information more transparent and clear[139]. This also helps to reflect the scientific production and operation mode of enterprises, strengthen the social responsibility of enterprises, promote the strategic goal of green development and sustainable development of enterprises, and establish a good corporate image for themselves.

4.8 Improve employees’ awareness of cost management

To enhance the effectiveness of construction cost management, construction enterprises need to emphasize the value and importance of cost management, fostering a culture of cost-consciousness and accountability[140]. Here are some key steps to achieve this: 1) Leadership and Accountability: It is the responsibility of the company’s management to be the first to acknowledge the importance of material cost management in engineering construction[141]. Management can innovate through several channels and assign tasks efficiently by prioritizing cost control. Developing a cost-management strategy that involves all parties and holds them accountable can promote effectiveness and efficiency. 2) Training and Awareness: Construction companies should place a high priority on encouraging cost management and stressing the value of cost consciousness among staff members. Employee comprehension and involvement with cost management procedures can be improved with regular management department-organized cost management training sessions[142]. Businesses can optimize the advantages of efficient cost management by fostering a culture that prioritizes cost consciousness and developing a sense of accountability for cost control at every level. 3) Continuous Learning and Improvement: In order to handle difficulties in construction cost management, staff members should actively develop their capacity for self-learning as well as continuously improve their management and customer service skills[143]. Employees can more successfully traverse the intricacies of cost management procedures and contribute to the overall success of cost management programs within the firm by supporting a culture of continuous improvement and skill development.

Through the discussion and research of the above measures, the relevant material cost management measures are provided to enterprises to help them start with different aspects of material management. From the aspects of material technology research and development, industrial technology sector innovation, the construction of material management systems, and the strengthening of employees’ economic awareness, we can help enterprises improve the cost management system of new green building materials, improve operational efficiency, and promote sustainable development in the highly competitive construction industry.

5. Conclusion and Future Direction

China’s future economic development is greatly aided by the low-carbon economy. China needs to take action to raise the cost control of new green building materials, increase economic efficiency, and boost market competitiveness in order to support the quick development of green construction.This study examines the key aspects and issues surrounding the price of new green construction materials in a low-carbon economy using a content analysis of 143 publications and papers. The goal of this study is to define the subtopics of the themes connected to these dimensions and then examine the primary aspects of the field of cost management of new green building materials; the majority of relevant research has mainly concentrated on the previous ten years. Finally, the shortcomings of the current research are summarized, and the future research direction and prospects are discussed.

Through the review of relevant journal papers, the value and significance of the new green building materials to the development of a low-carbon economy and the importance of the cost management of the new green building materials to the project cost are understood. In many articles, the main problems existing in the cost management of building materials are summarized. In conclusion, according to the problems, the cost management measures of new green building materials are discussed, and it is concluded that the cost management of new building materials can start with the raw materials, through the innovation of the technical department of the building materials’ industry, the use of technical means, renewable energy and other ways to carry out the research and development of new green building materials. Reduce the price of new green building materials from the source. In addition, construction enterprises and cost management personnel should always pay attention to the development of the construction industry under the new situation and establish a sound management system for the three stages of procurement, transportation, and warehousing of new building materials. To enhance the material price management visualization for new green building materials, establish a material price risk management method. In order to improve the material cost management system and strengthen the material cost management activities, standardize enterprise environmental accounting and raise staff awareness of cost management. This will provide new momentum for businesses that are focused on sustainable development.

However, the framework proposed by these initiatives may not fully include an integrated and holistic approach and will need to be further explored in future studies. Based on the recommendations derived from the developed framework, it is expected that future research in this area should prioritize in-depth research in the areas of material research and development, material management system deepening, environmental cost disclosure, and cost accounting system strengthening.

Authors contribution

Liao KY: Conceptualization, investigation, writing-original draft, writing-review & editing.

Zhang M, Zhang HX: Writing-review & editing.

Conflicts of interest

The authors declare there is no conflicts of interest.

Ethical approval

Not applicable.

Consent to participate

Not applicable.

Consent to publication

Not applicable.

Availability of data and material

Not applicable.

Funding

None.

Copyright

© The Author(s) 2024.

References

-

1. Pang ZH, Ding YQ. Large construction enterprises should change from extensive management to intensive management. Constr Econ. 1990;(07):19-20. Chinese. Available from: https://kns.cnki.net/kcms2/article/abstract?v=gR09I6yibQ5EAGWLNfc-vwI1N8LE2CGZ8neIZVPesLtw-iSCfp_5d1bsD4a1IEFcNO57ZUTQP1zYkF-vY_nsPMahIUcb4rqnwncT2axUhCQ7yBy-NMUkmAlzbH8ddviom0Cbw5gaYyA=&uniplatform=NZKPT&language=CHS

-

2. Zhang HK, Li YH. Comparison and application of energy saving and environmental protection building materials with traditional building materials. Splice. 2022;49(10):101-104. Chinese. Available from: https://kns.cnki.net/kcms2/article/abstract?v=gR09I6yibQ7RJaZa0I5LuAHDlqTwsqlS3PoQ9wTUfSRK_W8e57QGICuT2tpz5oI_nSggGrHqkxaG2eILrMhSaPkEBTLV1C20ZgmTV3U-bIaCp7OTGntoDrMeJ2vtEmTIjXur3F05qmX5QwiuCXKXIw==&uniplatform=NZKPT&language=CHS

-

3. Deng JX, Hu W. Research on incentive mechanism of green building development. Adv Mater Res. 2013;773:932-935.[DOI]

-

4. Li XM. Material price risk control in construction cost control. Mater Prot. 2020;53(10):175-176. Chinese.[DOI]

-

5. Ministry of Housing and Urban-Rural Development of the People’s Republic of China [Internet]. Green building evaluation criteria 2006. 2006. Available from: https://www.gov.cn/banshi/2006-05/12/content_278628.htm.

-

6. Ministry of Housing and Urban-Rural Development of the People’s Republic of China [Internet]. Green building evaluation criteria 2014. 2014. Available from: https://www.mohurd.gov.cn/gongkai/zc/wjk/art/2015/art_17339_224219.html

-

7. Ministry of Housing and Urban-Rural Development of the People’s Republic of China [Internet]. Green building evaluation criteria 2019. 2019. Available from: https://www.mohurd.gov.cn/gongkai/zc/wjk/art/2019/art_17339_240717.html

-

8. Liu J, Wang P, Li T, Ma G. Analysis of budget and cost control of new green building projects. J Archit Res Dev. 2018;2(4):35-38.[DOI]

-

9. Wu ZZ, Huang HQ, Chen XS, Li JJ, He QF, Li A, et al. Research on low-carbon transformation strategy of construction industry under the goal of “double carbon”. Chin Eng Sci. 2023;25(05):202-209. Chinese. Available from: https://kns.cnki.net/kcms2/article/abstract?v=64ENavj7QCAbbC0f7n8wiZZaGpL95oRK9tn6Ccl0rIW75CaepXbxCCO2QjVR0fVMcVFSCbsImqbdJb0nfnuzLyf1P-NZ9xioE2AfbnpjOqBQI5RYcuq_8f_VDRp6lHU1MoJXxAUWK4Nz2DvZEItVcNuiRIvgbp_5

-

10. Lin WH. Problems and countermeasures in project cost control of construction enterprises. J Shanxi Uni Finance and Econ. 2019;41(S2):69-70. Chinese. Available from: https://kns.cnki.net/kcms2/article/abstract?v=64ENavj7QCBEebf5Xsn8Zs0VwxAvukUCuQDTJJplX0mJyNyuFuLS7n3Jcx2vylaNVxZOfPwsrVNVuTihz7hwL52uRGlUhifm6uXTAbzkIRHaTNwX7NcYFsNgyVJuTIPv8M1JE8AwcaB5X0yNCqLtnMW3bw27Nkx5

-

11. Ma YL. Research on the development and challenge of building new material industry under the background of low-carbon economy. Ceramic. 2021;(07):116-117. Chinese.[DOI]

-

12. Işıkdag Ü, Hepsağ A, Bıyıklı S, Öz D, Bekdaş G, Geem Z. Estimating construction material indices with ARIMA and optimized NARNETs. Comput Mater Continua. 2023;74(1):113-129.[DOI]

-

13. Vedartham S, Sudarsan JS, Narayan V, Prasanna K, Mohanakrishna S. Cost-benefit analysis of adoption of green materials in conventional building to improve green rating. In: Gencel O, Balasubramanian M, Palanisamy T, editors. Sustainable Innovations in Construction Management. New York: Springer; 2024. p. 317-324.[DOI]

-

14. Giesekam J, Barrett JR, Taylor P. Construction sector views on low carbon building materials. Build Res Inf. 2015;44(4):423-444.[DOI]

-

15. Zhang ZY, ZhAng ZX. The construction and empirical study on evaluation index system of international low-carbon economy development. Fronti Energy Res. 2021;9:761567.[DOI]

-

16. Ruan M. Analysis of full lifecycle cost management of construction projects in the construction phase. Academic J Manage Soc Sci. 2024;7(1):1-3.[DOI]

-

17. Xu Y. Project cost control and management under low carbon concept. Low-carbon World. 2017;(28):255. Chinese.[DOI]

-

18. Eberhardt LCM, Birgisdottir H, Birkved M. Potential of circular economy in sustainable buildings. Mater Sci Eng. 2019;471(9):092051.[DOI]

-

19. Ajayabi A, Chen HM, Zhou K, Hopkinson P, Wang Y, Lam D. Rebuild: regenerative buildings and construction systems for a circular economy. Earth Environ Sci. 2019;225(1):012015.[DOI]

-

20. Li J, Yao T. Research on risk management of final accounts of capital construction projects from the perspective of internal control. In: Proceedings of the 2nd International Conference on Engineering Management and Information Science, EMIS 2023; 2023 Feb 24-26; Chengdu, China. Bratislava: European Alliance for Innovation. 2023.[DOI]

-

21. Ting W. Research on Operation Mode of Construction Project Tracking Audit Based on Work Process. In: Proceedings of the 2020 5th International Conference on Economics Development, Business & Management (EDBM 2020); 2020 Mar 23-25; Cologne, Germany. 2020.[DOI]

-

22. Zhang JL. Dynamic Control and Management of Construction Engineering Cost. IOP Conf Ser: Earth Environ Sci. 2021;638(1):012090.[DOI]

-

23. Cheng H. The significance and function of emphasizing construction cost management are discussed. Mod. 2020;(07):132-133. Chinese.[DOI]

-

24. Rahla KM, Mateus R, Bragança L. Selection criteria for building materials and components in line with the circular economy principles in the built environment - a review of current trends. Infrastructures. 2021;6(4):49.[DOI]

-

25. Ahmad TL, Susanty A. House of risk approach for assessing supply chain Risk management of material procurement in construction industry. IOP Conf Ser: Mater Sci Eng. 2019;598(1):012060.[DOI]

-

26. Lv R, Chen J, Sun Q, Ye Z. Design - construction phase safety risk analysis of Assembled Buildings. Buildings. 2023;13(4):949.[DOI]

-

27. Yang YN. How to promote comprehensive budget management of engineering projects in construction enterprises. In: Proceedings of the 2023 International Academic Forum on Finance and Management; 2023 Oct 11-14; Beijing, China. 2023.

-

28. Fisch JH, Ross JM. Timing product replacements under uncertainty - the importance of material - price fluctuations for the success of products that are based on new materials. J Prod Innovation Manage. 2014;31(5):1076-1088.[DOI]

-

29. Zhang ZW. Material price risk control in construction cost management. Stone. 2023;(04):57-59. Chinese.[DOI]

-

30. Ikechukwu FU. Investigation on the influence of building materials price fluctuation on cost of building products in Nigeria. Curr J Appl Sci Technol. 2021;40(2):118-130.[DOI]

-

31. Liu FF, You QS. Study on the influence of price fluctuation of main materials on construction cost of infrastructure engineering. Constr Econ. 2022;43(S1):241-244. Chinese.[DOI]

-

32. Zhong GF. The influence of new green building materials on construction cost management. Ceramic. 2023;(03):191-193. Chinese.[DOI]

-

33. Zhu N, Yang B, Zhang ZX, Wang MJ. Application of BIM in green building materials management. J Physics: Conference Series. IOP Publishing. 2021;1986(1):012024.[DOI]

-

34. Junussova T, Nadeem A, Kim JR, Azhar S. Key Drivers for BIM-Enabled Materials Management: Insights for a Sustainable Environment. Buildings. 2023;14(1):84.[DOI]

-

35. Wang X. Application analysis of BIM technology in building engineering design. Jiangxi Build Mater. 2022;(10):159-160. Chinese. Available from: https://kns.cnki.net/kcms2/article/abstract?v=gR09I6yibQ6JzSwrBymtHqxKWsbp0-oidZvP2vo0F6R8lSBIb_ggOz5p3gtX9tIUjuA8Ax_hI3Y8B4iRLTdXrlDtT8-l_P-GYhjR_xUKd7-mNuihVnOJJNvDukYOOwvN6nZOJYzmkiwQuHd7845YTQ==&uniplatform=NZKPT&language=CHS

-

36. Zhao H, Wang Y, Qiu W, Qu W, Zhang X. Research on the application of green building materials in China. IOP Conf Ser: Earth Environ Sci. IOP Publishing. 2018;186(2):012043.[DOI]

-

37. Xia LJ. Research on construction supply chain management strategy based on storage and transportation optimization. Logist Purchasing China. 2024;(06):61-62. Chinese.[DOI]

-

38. Yan YM. Analysis of the existing problems and countermeasures in the testing of building construction materials. Eng Technol Manage. 2024;8(3). Chinese.[DOI]

-

39. Thunberg M, Rudberg M, Karrbom Gustavsson T. Categorising on-site problems: a supply chain management perspective on construction projects. Constr Innovation. 2017;17(1):90-111.[DOI]

-

40. Lu H, Wang H, Qi C, Xie Y, Liu D. Incentive schemes for centralized material planning and allocation with asymmetric information in construction supply chain. IEEE Access. 2025;13:124763-124775.[DOI]

-

41. Shishehgarkhaneh MB, Moehler RC, Fang Y, Aboutorab H, Hijazi AA. Construction supply chain risk management. Auto Constr. 2024;162:105396.[DOI]

-

42. Pham HT, Pham T, Truong Quang H, Dang CN. Supply chain risk management research in construction: a systematic review. Interl J Constr Manage. 2023;23(11):1945-1955.[DOI]

-

43. Chen HD, Li X, Yu CZ, He M, Liu ZS, Tong L. Safety monitoring twin system of three large foundation pits based on Internet of Things technology. Ind Constru. 2024;54(5):1-8. Chinese.[DOI]

-

44. Bonci A, Carbonari A, Cucchiarelli A, Messi L, Pirani M, Vaccarini M. A cyber-physical system approach for building efficiency monitoring. Auto Constr. 2019;102:68-85.[DOI]

-

45. Garyaev N, Garyaeva V. Big data technology in construction. E3S Web Conf. 2019;97(4):01032.[DOI]

-

46. Zeng Z, Wei Y, Wei Z, Yao W, Wang C, Huang B, et al. Deep learning enabled particle analysis for quality assurance of construction materials. Auto Constr. 2022;140:104374.[DOI]

-

47. Khoshnevis B, Hwang D, Yao KT, Yeh Z. Mega-scale fabrication by contour crafting. Interl J Ind Syst Eng. 2006;1(3):301-320.[DOI]

-

48. Xu Z, Fan W, Duan J, Xia Y, Nie Z, Sui K. Construction of 3D Shape - Changing Hydrogels via Light - Modulated Internal Stress Fields. Energy Environ Mater. 2023;6(3):e12375.[DOI]

-

49. Weger D, Gehlen C, Korte W, Meyer-Brötz F, Scheydt J, Stengel T. Building rethought - 3D concrete printing in building practice. Constr Robot. 2021;5(3):203-210.[DOI]

-

50. Dixit MK. 3-D printing in building construction: a literature review of opportunities and challenges of reducing life cycle energy and carbon of buildings. IOP Conf Ser: Earth Environ Sci. 2019;290(1):012012.[DOI]

-

51. Chel A, Kaushik G. Renewable energy technologies for sustainable development of energy efficient building. Alexandria Eng J. 2018;57(2):655-669.[DOI]

-