How digital transformation empowers building and real estate enterprises to enhance new quality productive forces?

*Correspondence to:

Yun Zhong, School of Management Science & Real Estate, Chongqing University, Chongqing 400044, China.

E-mail: zhongyun@cqu.edu.cn

J Build Des Environ. 2026;4:2025123. 10.70401/jbde.2026.0036

Received: November 29, 2025Accepted: April 08, 2026Published: April 09, 2026

This article belongs to the Special lssue Digital Transformation in Construction: Innovations and Challenges

Abstract

Developing new quality productive forces (NQPFs) in the building and real estate industry is essential for sustainable economic growth. Utilizing panel data on Chinese A-share listed building and real estate companies from 2011 to 2024, this study empirically investigates the impact of digital transformation (DT) on corporate NQPFs and the underlying mechanisms. Our baseline findings confirm that DT exerts a significantly positive effect on NQPFs, effectively overcoming the “Solow Paradox” in this capital-intensive sector. Moving beyond this initial assessment, the study systematically unpacks the mechanisms underlying digital value creation. We reveal that DT promotes the enhancement of NQPFs through three core mechanisms: fostering technological innovation, upgrading the human capital structure, and improving asset operational efficiency. Furthermore, the multidimensional heterogeneity analysis demonstrates that this digital empowerment is highly context-dependent. The enabling effect is significantly more pronounced in the Eastern and Central regions and is amplified by stronger intellectual property protection, more advanced digital infrastructure, state ownership, and larger firm size. By elucidating these specific pathways, this research offers targeted guidelines for sector-specific digital policy-making and strategies to optimize corporate NQPFs.

Keywords

Digital transformation, new quality productive forces, high quality development

1. Introduction

Current global technological progress and industrial transformation exhibit strong mutual reinforcement, and productivity is undergoing a historic leap. At the same time, China’s macroeconomy faces severe development bottlenecks. The traditional growth model, heavily reliant on resource consumption, demographic dividends, and large-scale capital expansion, is losing momentum amid shifting global dynamics, structural imbalances, and rising resource and environmental constraints[1]. To overcome these challenges and achieve sustainable growth, the concept of new quality productive forces (NQPFs) is reshaping the corporate growth paradigm. The characteristics of NQPFs can be summarized in two key aspects. Theoretically, NQPFs represent a higher-order form of productivity in which innovation acts as the primary driver, breaking away from conventional approaches to economic expansion and production trajectories; they are characterized by advanced technologies, higher efficiency, and superior quality, consistent with the new development philosophy[2]. Practically, fostering NQPFs is a fundamental prerequisite and central task for promoting high-quality development; it is therefore vital to prioritize innovation and accelerate the development of NQPFs[3]. Consequently, NQPFs have emerged as a crucial concept for understanding the new drivers of China’s economic growth and for guiding sectoral restructuring and modernization through applied innovation. As a vital component of the Chinese economy, the building and real estate industry currently acutely affected by these macroeconomic structural adjustments, must accurately understand NQPFs and implement their core tenets in practice, making this a critical issue that demands in-depth analysis.

Unlike the traditional economy, the digital economy breaks the time and space constraints on interactions among economic entities through mechanisms such as resource sharing and inclusive, mutually beneficial cooperation, fundamentally transforming the pattern and structure of economic development[4,5]. According to official statistics, China’s digital economy reached 63.8 trillion yuan in 2024, accounting for nearly half of the country’s total economic output, and has emerged as a critical pillar of the qualitative upgrading of China’s economy. In the context of digital economic development, digital transformation (DT) is a central theme and an imperative for firms’ sustainable operations and growth, while accelerating corporate DT has become a centerpiece of digital economy growth. With the widespread adoption of foundational digital technologies, DT has opened new avenues for restructuring and long-term development in the building and real estate industry. Building and real estate companies are increasingly integrating DT into core processes such as design, construction, and operations, thereby reshaping their production processes and management practices[6]. Against this backdrop, assessing the impact of DT on NQPFs in building and real estate companies is critical for enabling the industry to seize emerging digital opportunities and explore new frontiers of economic growth.

The existing literature exhibits three key limitations. First, most studies investigating DT and NQPFs focus on general industries and fail to narrow their research to specific sectors[7,8]. Whether the “Solow Paradox” of the digital era, where the adoption of new technologies fails to enhance NQPFs, applies to China’s socialist market economy, particularly in the building and real estate industry, remains untested. Second, there is a lack of in-depth exploration into the mechanisms through which DT affects NQPFs, especially those specific to the industry’s unique operational characteristics. Finally, existing studies on the economic effects of DT often fail to adequately incorporate heterogeneous external environments and internal firm characteristics as moderating variables, which limits the understanding of the conditional boundaries of these effects and weakens their practical implications for managerial practice.

This study addresses three core questions: First, what is the impact of DT on the NQPFs of building and real estate companies, and how can this relationship be empirically assessed? Second, how does DT influence NQPFs in these companies, given the industry’s unique operational characteristics? Third, does this effect vary significantly across different external environments and internal conditions, particularly regarding regional distribution, intellectual property protection, digital infrastructure, ownership types, and firm sizes? Using panel data from Chinese A-share listed building and real estate companies from 2011 to 2024, this study investigates the effect of DT on NQPFs and explores its transmission mechanisms. A series of endogeneity and robustness tests were then conducted, including controlling for joint fixed effects, applying the instrumental variables (IV) approach, using the difference-in-differences (DID) method, replacing the dependent and core explanatory variables, and performing subsample regressions. Finally, the study examines how the effects of DT on NQPFs differ across various macro-level external environments and internal firm characteristics.

The findings are as follows: First, DT drives productivity towards “novelty” and “quality”, significantly promoting the development of NQPFs in building and real estate companies. Second, in terms of transmission mechanisms, DT enhances NQPFs in these companies by boosting innovation capacity, optimizing human capital, and improving asset operational efficiency. Third, both external factors such as intellectual property protection and digital infrastructure, and internal firm characteristics like state ownership and large firm size, amplify the positive effect of DT on NQPFs. Fourth, from a regional perspective, DT significantly promotes NQPFs in the Eastern and Central regions, while this effect is not yet observable in the Western region.

The core contributions of this study are threefold. First, it tests the digital-era “Solow Paradox” in the unique context of China’s large, transitioning building and real estate sector. By quantifying the effect of DT on NQPFs, it provides new evidence on how traditional, capital-intensive industries can achieve high-quality development amid structural macroeconomic shifts. Second, it identifies sector-specific transmission mechanisms, showing how DT drives value creation through innovation, human capital optimization, and asset operational efficiency. Third, it clarifies the boundary conditions of digital empowerment by leveraging China’s distinct institutional and spatial characteristics. By systematically examining spatial geography (Eastern and Central regions compared to the Western region), external macro-environments (intellectual property protection and digital infrastructure), and internal organizational traits (state ownership and firm size), this multidimensional analysis highlights the contextual dependencies of DT. Ultimately, China’s pioneering digital practices within this sector offer important international implications, providing a scalable blueprint for other emerging economies seeking to modernize traditional industries and formulate effective digital economy policies.

The remainder of this study is structured as follows: Section 2 reviews the literature and presents the theoretical framework and research hypotheses; Section 3 outlines the research design; Section 4 presents and discusses the empirical results; and Section 5 concludes the study.

2. Literature Review

2.1 Literature review on DT and NQPFs

Existing academic literature examines the pathways and economic effects of corporate DT. DT is defined as the process triggered by the combination of information, computing, communication, and connective technologies, leading to profound shifts in organizational characteristics and driving transformation[9]. Regarding the pathways, internally, executives’ career experiences in digital technology facilitate knowledge sharing and corporate DT[10]. Externally, tax incentives, government digital procurement, and subsidies collectively encourage corporate DT[11,12]. Digital economy regulation supports corporate DT by maintaining competitive order, facilitating the mobility of digital talent, and fostering innovation[13]. In terms of economic consequences, DT positively impacts knowledge creation[14], total factor productivity (TFP)[8], green TFP[15], financing efficiency[16], stock liquidity[17], human capital structure[18], labor demand[19], export stability[20], internal control[21], risk-taking levels[22], analyst coverage[23], audit efficiency[24], ESG performance[25], environmental responsibility[26], innovation[27], digital technology innovation[28], green innovation[29], operational performance[30], sustainable development[31], and merger and acquisition activities[32]; conversely, DT negatively affects stock price crash risk[33], carbon emissions[34], debt financing costs[35], debt default risk[36], R&D manipulation[37], major customer dependency[38], policy uncertainty perceptions[39], the maturity mismatch between investment and financing[40], and financial restatements[41].

Existing research primarily focuses on elucidating the connotations and factors influencing corporate NQPFs. The theoretical interpretation and logical structure of NQPFs can be organized around three dimensions: first, at the level of technological breakthroughs, they measure new productivity drivers by leveraging changes driven by sectoral advancement and technical innovation[2]; second, at the level of innovative allocation of production factors, they identify innovation-driven forces by drawing on the “new” in technology, economics, and business models, as well as the “quality” in key technological breakthroughs[2]; third, at the level of industrial evolution, they emphasize the new industrial ecology formed by intersectoral integration[42]. Specifically, new quality laborers are employees with high technical proficiency, strong learning capabilities, and substantial R&D and innovation skills, capable of mastering new quality means of production[43]; new quality means of production include high-precision equipment, artificial intelligence, and industrial robots, which promote sustainable corporate development through low-input, high-output factor utilization[44]; and new quality objects of labor extend beyond traditional assets to include the economic benefits of pervasive factors such as data[45]. The emergence of NQPFs stems from three key dimensions: first, at the level of driving forces, they focus on high technology to accelerate technological breakthroughs[3]; second, at the level of implementation pathways, they focus on high performance to promote the innovative allocation of production factors[46]; third, at the level of transformation carriers, they focus on high quality to foster deep industrial transformation and upgrading[3].

Existing research examines the relationship between DT and firm productivity, yielding two divergent conclusions. Some researchers argue that corporate DT positively impacts productivity by alleviating information asymmetry[47], improving factor allocation efficiency[48], enhancing production and operational efficiency[49], and reducing both internal governance costs[7] and external transaction costs[50]. In contrast, other scholars disagree. Solow found that the invention and use of new technologies were not reflected in productivity statistics, a phenomenon known as the “Solow Paradox”[51]. Brynjolfsson et al. observed that the rapid advancement of digital technologies over the past decade coincided with a slowdown, or even stagnation, in TFP growth across major economies, creating a new “Solow Paradox” in the digital age[52]. In summary, scholars have yet to reach a consensus on whether DT enhances firm productivity, and they have largely neglected specific industries. Unlike traditional productivity, NQPFs are defined by “the leapfrogging of laborers, means of labor, objects of labor, and their optimal combination, with a substantial increase in TFP as their key marker; they are characterized by innovation, quality, and advanced productive forces”[53]. Whether DT can genuinely foster “novelty” and “quality” to advance NQPFs in the building and real estate sectors requires further systematic investigation.

Although previous research has yielded significant findings, it still has three key limitations. First, most studies focus on general industries, where differences in institutional environments and firm characteristics lead to divergent conclusions about the relationship between DT and production efficiency, leaving the existence of the digital-era “Solow Paradox” untested in specific contexts. Second, there is a lack of comprehensive investigation into specific sectors, such as the building and real estate industry, and insufficient systematic exploration of the mechanisms through which DT impacts NQPFs, particularly those related to industry-specific operational characteristics. Third, prior studies examining the economic consequences of DT do not adequately incorporate contextual variables, failing to clarify the conditional boundaries of these heterogeneous effects. The core innovations of this study are as follows: First, it focuses on the building and real estate industry and precisely identifies the impact of DT on the NQPFs of these companies through empirical analysis. Second, from the perspectives of “innovation-driven”, “human capital”, and “asset operation”, it unpacks the mechanisms between the two. Third, it examines the heterogeneous moderating effects of “regional distribution”, “intellectual property protection”, “digital infrastructure development”, “ownership type”, and “firm size” on their relationship, providing insights for policymakers to accelerate the development of both the “soft” and “hard” environments underpinning DT.

2.2 Theoretical analysis and hypothesis development

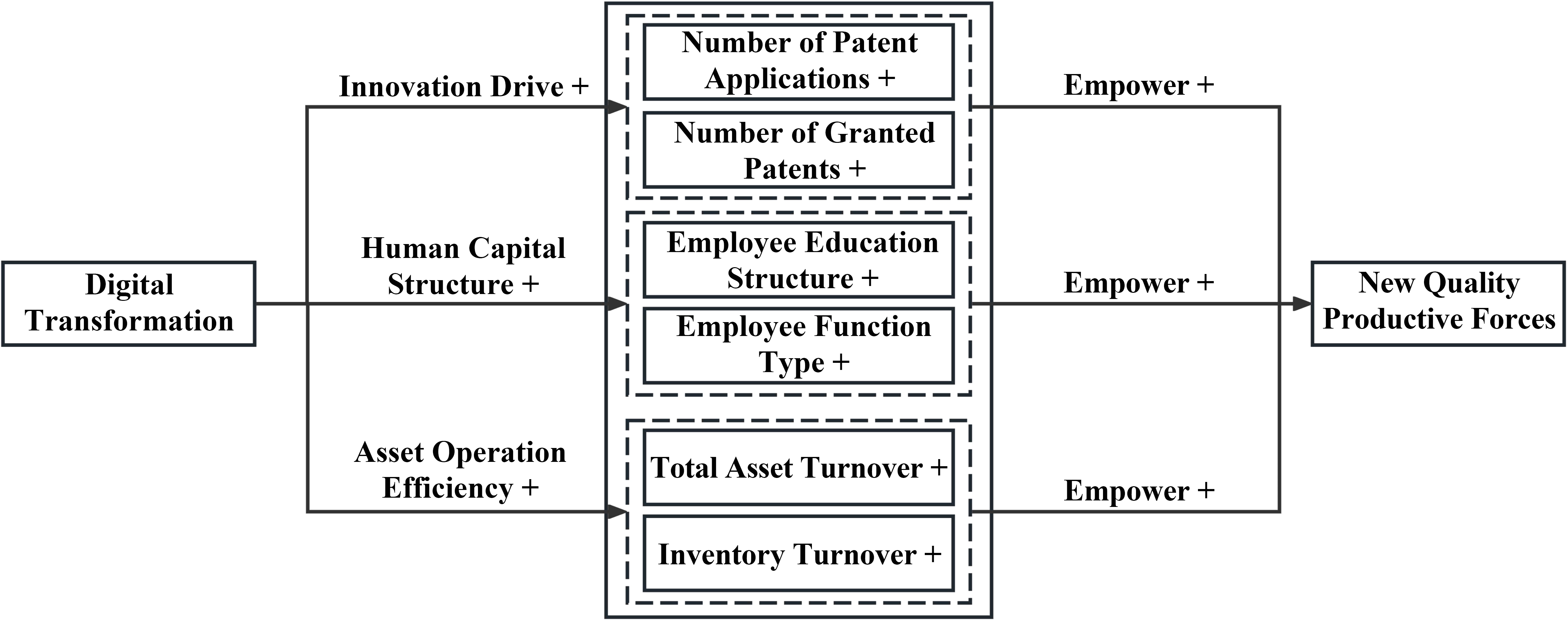

From the perspective of the three core dimensions of NQPFs, the characteristics of DT in building and real estate companies align closely with NQPFs. Regarding labor, new quality laborers compatible with NQPFs are knowledge-based, innovative workers who require more advanced cognitive and professional skills than traditional laborers and can proficiently apply cutting-edge technologies and intelligent equipment in production[43]. Building and real estate companies undergoing DT rely on high-quality digital talent[54], which simultaneously increases the demand for skilled labor while replacing some routine, repetitive low-skilled positions[55], thus creating a talent pool to support NQPFs improvement. Regarding the means of labor, the means required by NQPFs include high-precision and sophisticated equipment that enhances the efficiency and quality of the supply system. By introducing intelligent equipment, building and real estate companies undergoing DT achieve significant improvements in production efficiency and resource utilization, making such equipment a core tool for technological innovation and production optimization[56]. Regarding the objects of labor, data elements are new objects of labor that drive NQPFs advancement. When data elements reach a certain scale, they significantly boost productivity without incurring additional costs for this effect[57]. In building and real estate companies undergoing DT, the objects of labor primarily consist of high-quality structured and unstructured data, which facilitate NQPFs improvement through continuous collection, analysis, and intelligent transformation, thus becoming a core competitive resource for these firms[58].

Building on the preceding theoretical analysis, this study proposes the following hypothesis: H1: DT drives the advancement of NQPFs in building and real estate companies.

Innovation drive is the core driver and distinctive feature of NQPFs[3]. From the perspective of underlying digital technologies in DT, artificial intelligence enriches and expands firms’ knowledge bases, helping building and real estate companies overcome technical barriers and achieve diversified technology layouts and cross-domain innovation[59]. NQPFs are fundamentally characterized by a substantial increase in TFP[46], and blockchain, recognized as a high-quality technological innovation, strongly facilitates TFP growth in building and real estate companies[60]. Cloud computing aids these companies in shortening innovation cycles and reducing R&D risks through iterative innovation models, thereby improving innovation efficiency[61]. Big data enables the convergence of talent, technology, capital, and data factors, optimizing the enterprise innovation ecosystem and significantly enhancing innovation quality in building and real estate companies[62]. Furthermore, internet connectivity eliminates time and space constraints on internal and external communication, boosting innovation openness and capability[63]. Digital technologies leverage their connectivity, aggregation, and analytical capabilities to foster high-end disruptive innovation through digital collaboration[64]. DT accelerates firm-level informatization processes, enhances the technological innovation capabilities of building and real estate companies[65], and promotes the advancement of NQPFs. In addition, it accelerates data flow and sharing within companies[8], facilitating the continuous improvement of NQPFs.

Building on the preceding theoretical analysis, this study proposes the following hypothesis: H2: DT drives the advancement of NQPFs in building and real estate companies by enhancing innovation capability.

NQPFs are fundamentally characterized by “the leapfrogging of laborers, means of labor, objects of labor, and their optimal combination”[66], and DT inevitably leads to changes in production methods and relations[55]. On the one hand, the new wave of technological progress brought by DT can eliminate most standardized, repetitive physical tasks, reducing reliance on low-skilled workers in production processes[48,67], creating a “technology substitution” effect, and driving the iterative advancement of NQPFs. On the other hand, as DT progresses, production technologies, machinery, and equipment are continuously upgraded, requiring building and real estate companies to equip themselves with specialized, high-skilled talent[8,68]. This results in a steady increase in the proportion of high-skilled labor, creating a “technology complementarity” effect and injecting sustained innovation momentum into NQPFs. Simultaneously, DT drives the expansion of business operations in building and real estate companies[68], creating more high-skilled positions, generating a “scale expansion” effect, and supporting the leapfrogging advancement of NQPFs. Ye et al. observed that the deep integration of digital systems with core business activities inevitably leads to capital deepening in companies; in this process, the increased demand for non-routine, high-skilled labor in building and real estate companies creates additional high-skilled jobs, optimizing the firms’ human capital structure[69].

Building on the preceding theoretical analysis, this study proposes the following hypothesis: H3: DT drives the advancement of NQPFs in building and real estate companies by optimizing the human capital structure.

DT significantly enhances enterprise operational efficiency, enabling building and real estate companies to maximize output within given resource constraints[70]. It facilitates mutual empowerment between digital technologies and traditional production factors, thereby improving the utilization of existing production factors[71]. DT permeates the design, management, and analytical processes of modern building and real estate operations, holding considerable potential to boost operational efficiency[72]. It accelerates internal information flow within these companies, ensuring resources are allocated to the most critical departments and optimizing overall resource allocation[47,73]. Furthermore, DT enhances communication between employees and functional units, promoting smooth information flow and resource sharing across departments[47]. As production tools enter the digital era, smart hardware collects data via interconnected networks, while software systems perform data-driven analytics and automated decisions, significantly improving production efficiency[8]. By leveraging digital technologies to manage large-scale, unstructured, and irregular data both internally and externally, building and real estate companies use this information for decision-making and market trend forecasting, optimizing production processes[17]. With data acquired through digital technologies, these companies can swiftly improve production processes and adjust plans, thereby enhancing asset operational efficiency[7]. DT not only boosts operational efficiency but also transforms management processes through demand creation, business design, value co-creation, supply chain restructuring, and ecosystem development, driving innovation in operational management models[74].

Building on the preceding theoretical analysis, this study proposes the following hypothesis: H4: DT drives the advancement of NQPFs in building and real estate companies by enhancing asset operational efficiency.

Building on the preceding theoretical analysis, this study presents a theoretical framework to illustrate how DT influences the NQPFs of building and real estate companies, as shown in Figure 1.

3. Research Design

3.1 Sample selection

This study selected Chinese A-share listed building and real estate companies from 2011 to 2024 as the sample. The raw data was sourced from the CSMAR database. To ensure the reliability and validity of the empirical results, the sample selection adhered to the following criteria: (1) exclusion of special treatment (ST and *ST) companies, as their abnormal financial status and operational distress could distort productivity estimates; (2) exclusion of firms with total assets less than total liabilities (insolvent firms), as their capital structures do not reflect typical industry operations; and (3) exclusion of firms with missing key financial data to ensure the accuracy of the panel data analysis. After applying these data cleaning procedures, the final sample comprised 211 listed building and real estate companies. Additionally, to address potential estimation bias from extreme outliers, winsorizing was applied at the 1st and 99th percentiles for all continuous variables.

3.2 Variable definitions

3.2.1 NQPFs

TFP represents the portion of output growth unexplained by the accumulation of traditional inputs, such as labor and capital, effectively capturing a firm’s technological progress, resource allocation efficiency, and overall innovation capacity. The concept of NQPFs, a paradigm increasingly central to China’s economic development strategy, aligns closely with TFP. Both frameworks prioritize qualitative growth driven by efficiency improvements over resource-intensive, quantitative expansion. However, NQPFs extend beyond the traditional boundaries of TFP by emphasizing breakthrough technological innovation, high-quality human capital accumulation, and the deep integration of advanced digital technologies. Despite these broader connotations, the core characteristic of NQPFs remains significant growth in TFP[46]. Consequently, this study used TFP as a robust quantitative proxy to assess the NQPF levels of building and real estate companies. Specifically, we applied the Levinsohn-Petrin (LP) and Olley-Pakes (OP) methods to estimate the TFP of the sample firms. Additionally, to verify the reliability of our baseline findings, we used several alternative estimation techniques in the robustness checks.

3.2.2 DT

This study used the corporate DT index calculation method from the CSMAR China Listed Company Digital Transformation Research Database. Based on disclosures such as annual reports, capital raising announcements, and qualification certifications, we developed a DT evaluation framework encompassing six dimensions: strategic guidance, technology-driven initiatives, organizational empowerment, environmental support, digital achievements, and application outcomes. In contrast to most studies that rely on annual reports or the “Management’s Discussion and Analysis” sections to measure DT by the frequency of digital terms[8,17], our data enables a more rigorous and comprehensive assessment of DT levels in building and real estate companies.

3.2.3 Control variables

Drawing on Huang et al. and Guo et al.[7,75], this study included a set of control variables that may influence the NQPFs of building and real estate companies. Specifically, these variables are firm age (Age), growth rate (Growth), financial leverage (Leverage), firm size (Size), market value (Tobin), profitability (Return), current ratio (Liquid), cash flow (Cashflow), and R&D investment (RDinvest). The definitions of these variables are provided in Table 1.

Table 1. Variable definitions.

| Variable Types | Variable Names | Variable Symbols | Variable Descriptions |

| Explained Variables | New Quality Productive Forces | TFP_LP | LP Method |

| TFP_OP | OP Method | ||

| Explanatory Variable | Digital Transformation | Digital | Corporate Digital Transformation Index |

| Mediating Variables | Patent Applications | Apply | Natural Logarithm of Number of Patent Applications |

| Granted Patents | Grant | Natural Logarithm of Number of Patents Granted | |

| Education Structure | Staff_Edu | Proportion of Employees with a Bachelor’s Degree or Higher | |

| Tech Staff Ratio | Staff_Tech | Proportion of Technical Staff Among Total Employees | |

| Total Asset Turnover | Asset_Turn | Total Asset Turnover Ratio | |

| Inventory Turnover | Stock_Turn | Inventory Turnover Ratio | |

| Heterogeneity Variables | Regional Factor | Region | 1 for Eastern Region, 2 for Central Region, 3 for Western Region |

| Intellectual Property | IP | 1 if Provincial IP Protection Index > Annual Median, 0 Otherwise | |

| Digital Infrastructure | Infra | 1 if Broadband Access Ports Ratio > Annual Median, 0 Otherwise | |

| Ownership Type | SOE | 1 if Actual Controller is State-owned, 0 Otherwise | |

| Firm Scale | Scale | 1 if Firm Size > Annual Industry Median, 0 Otherwise | |

| Control Variables | Firm Age | Age | Natural Logarithm of Firm Age |

| Growth Rate | Growth | Operating Revenue Growth Rate | |

| Financial Leverage | Leverage | Total Liabilities/Total Assets | |

| Firm Size | Size | Natural Logarithm of Number of Employees | |

| Market Value | Tobin | Total Market Value/Total Assets | |

| Profitability | Return | Net Profit/Operating Revenue | |

| Current Ratio | Liquid | Current Assets/Total Assets | |

| Cash Flow | Cashflow | Net Cash Flow from Operating Activities/Total Assets | |

| R&D Investment | RDinvest | R&D Expenditure/Operating Revenue |

TFP: total factor productivity; LP: Levinsohn-Petrin; OP: Olley-Pakes; IP: intellectual property; SOE: state-owned enterprise.

3.3 Model construction

To rigorously test the effect of DT on NQPFs and mitigate potential omitted variable bias, this study employed a two-way fixed effects (TWFE) regression model as the baseline. The TWFE model was selected because it controls for unobservable, time-invariant firm characteristics (via firm fixed effects) and macro-environmental shocks affecting all firms simultaneously (via year fixed effects). Thus, this study constructed the following econometric regression model.

In Equation (1), i denotes a building and real estate enterprise, and t denotes the year. TFPi,t and Digitali,t represent the NQPF and the DT index of enterprise i in year t, respectively. Zi,t represents a set of control variables, while δi and μt denote firm and year fixed effects, respectively. Additionally, this study clustered the standard errors at the firm level.

4. Empirical Results and Discussion

4.1 Descriptive statistics

Table 2 shows that the mean value of DT (Digital) is 33.726, with a standard deviation of 7.01, indicating significant variation in the degree of DT across building and real estate companies. The mean values of NQPFs (TFP_LP, TFP_OP) are 10.039 and 7.697, respectively, which are generally consistent with prior literature[7]. All other variables fall within reasonable ranges.

Table 2. Descriptive statistics of variables.

| VarName | Obs | Mean | SD | Min | Median | Max |

| TFP_LP | 1,555 | 10.039 | 1.217 | 6.069 | 9.992 | 12.327 |

| TFP_OP | 1,555 | 7.697 | 0.869 | 4.713 | 7.748 | 9.490 |

| Digital | 1,555 | 33.726 | 7.010 | 23.530 | 32.749 | 52.834 |

| Age | 1,555 | 3.103 | 0.317 | 1.946 | 3.135 | 3.714 |

| Growth | 1,555 | 0.166 | 0.600 | -0.804 | 0.088 | 6.261 |

| Leverage | 1,555 | 0.677 | 0.169 | 0.139 | 0.718 | 0.946 |

| Size | 1,555 | 7.968 | 1.706 | 3.611 | 7.684 | 12.484 |

| Tobin | 1,555 | 1.295 | 0.626 | 0.785 | 1.111 | 8.670 |

| Return | 1,555 | 0.012 | 0.274 | -2.601 | 0.043 | 0.623 |

| Liquid | 1,555 | 0.755 | 0.156 | 0.146 | 0.789 | 0.985 |

| Cashflow | 1,555 | 0.009 | 0.064 | -0.245 | 0.011 | 0.244 |

| RDinvest | 1,555 | 0.018 | 0.018 | 0.000 | 0.013 | 0.089 |

TFP: total factor productivity; LP: Levinsohn-Petrin; OP: Olley-Pakes; SD: standard deviation.

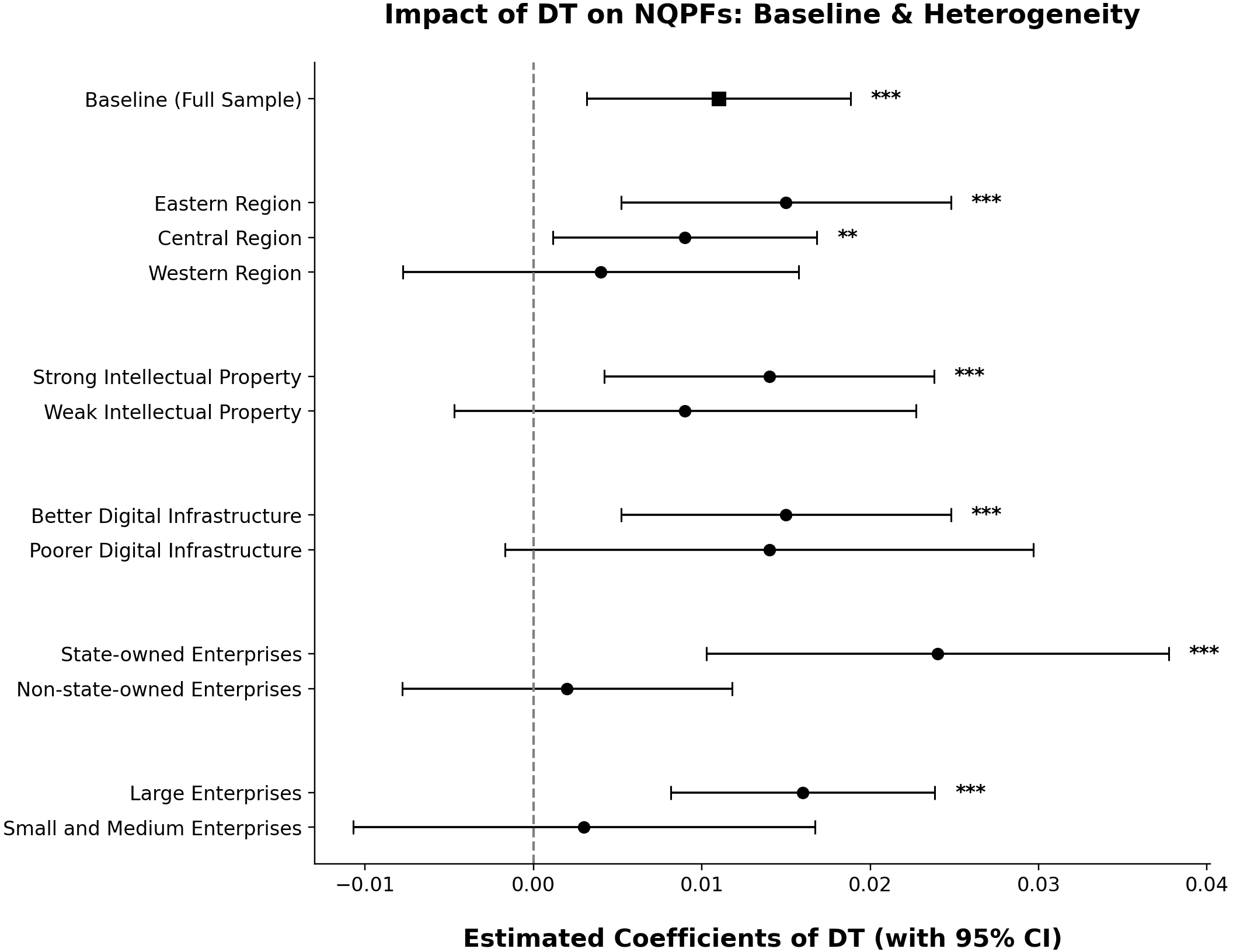

4.2 Baseline regression tests

Columns (1) and (2) of Table 3 include firm and year fixed effects. The coefficients of DT on NQPFs are significantly positive, indicating that building and real estate companies implementing DT show higher NQPFs on average. Columns (3) and (4) incorporate a set of control variables. The regression coefficient of DT is 0.011, representing a substantial increase in the NQPFs of building and real estate companies. Therefore, the effect of DT on the growth of NQPFs in these companies is both statistically and economically significant.

Table 3. Baseline regression tests.

| Variables | (1) | (2) | (3) | (4) |

| TFP_LP | TFP_OP | TFP_LP | TFP_OP | |

| Digital | 0.017*** (0.005) | 0.010** (0.005) | 0.011*** (0.004) | 0.011*** (0.004) |

| Age | 0.286 (0.254) | 0.387* (0.234) | ||

| Growth | 0.147*** (0.021) | 0.143*** (0.020) | ||

| Leverage | 1.026*** (0.178) | 1.098*** (0.174) | ||

| Size | 0.323*** (0.052) | 0.015 (0.054) | ||

| Tobin | -0.130*** (0.038) | -0.119*** (0.037) | ||

| Return | 0.597*** (0.057) | 0.601*** (0.055) | ||

| Liquid | 1.540*** (0.163) | 1.404*** (0.157) | ||

| Cashflow | 0.507** (0.203) | 0.464** (0.190) | ||

| RDinvest | -7.814*** (1.823) | -7.759*** (1.966) | ||

| _cons | 9.464*** (0.176) | 7.375*** (0.158) | 4.616*** (0.950) | 4.470*** (0.904) |

| Firm | YES | YES | YES | YES |

| Year | YES | YES | YES | YES |

| Observations | 1,555 | 1,555 | 1,555 | 1,555 |

| adj.R2 | 0.862 | 0.791 | 0.933 | 0.877 |

Robust standard errors are shown in parentheses. Statistical significance at the 1%, 5%, and 10% levels is indicated by ***, **, and *, respectively. This convention applies to all subsequent tables. TFP: total factor productivity; LP: Levinsohn-Petrin; OP: Olley-Pakes.

4.3 Endogeneity tests

4.3.1 Controlling for joint fixed effects

The residual term in the baseline regression model may include factors that simultaneously affect both DT and NQPFs, leading to biased estimates of the regression coefficients. Specifically, omitted variables such as regional policy support and industry-level trade shocks may be present. Therefore, this study controlled for province × year and industry × year interaction terms. Across all specifications in Table 4, the coefficients of DT remain statistically significant at the 5% level. Thus, the conclusions remain robust after accounting for systematic changes in the external environment.

Table 4. Controlling for joint fixed effects.

| Variables | (1) | (2) | (3) |

| TFP_LP | TFP_LP | TFP_LP | |

| Digital | 0.011** (0.005) | 0.011** (0.005) | 0.012** (0.005) |

| Controls | YES | YES | YES |

| Province | NO | YES | NO |

| Industry | YES | NO | NO |

| Province × year | YES | NO | YES |

| Industry × year | NO | YES | YES |

| Observations | 1,764 | 1,848 | 1,753 |

| adj.R2 | 0.757 | 0.770 | 0.761 |

TFP: total factor productivity; LP: Levinsohn-Petrin.

4.3.2 IV approach

First, this study constructed an IV using postal and telecommunications data. Well-established postal and telecommunications infrastructure promotes DT in building and real estate companies[55]. The study used the fixed-line telephone penetration rate in the 1980s as a proxy for the development level of postal and telecommunications services. The rationale is that fixed-line dial-up was the primary network access method in China, and the historical fixed-line telephone penetration rate across regions reflects the development of the postal and telecommunications industry[76], which is significantly correlated with local firms’ DT levels[55]. Meanwhile, the frequency of fixed-line telephone use in daily operations has significantly declined and no longer affects NQPFs, thus satisfying the exclusion restriction of the IV[77]. Since this historical data is cross-sectional and cannot be used as an IV in models with firm fixed effects, the study constructed an interaction term using a relevant time-series variable. Specifically, it interacted the number of internet broadband access ports in the province where building and real estate companies are located with the natural logarithm of the number of fixed-line telephones per hundred people in 1984 in the prefecture-level city where these companies are currently located, using the resulting interaction term as the IV Telephone. Columns (1) and (2) of Table 5 report the estimation results, both confirming the core conclusion of this study.

Table 5. Instrumental variables approach and difference-in-differences method.

| Variables | (1) | (2) | (3) | (4) | (5) |

| Digital | TFP_LP | Digital | TFP_LP | TFP_LP | |

| Telephone | 0.001*** (0.000) | ||||

| Digital_Average | 0.940*** (0.069) | ||||

| Digital | 0.085*** (0.031) | 0.023*** (0.007) | |||

| Broadband | 0.162*** (0.061) | ||||

| Controls | YES | YES | YES | YES | YES |

| Firm | YES | YES | YES | YES | YES |

| Year | YES | YES | YES | YES | YES |

| Observations | 1,584 | 1,584 | 1,860 | 1,860 | 1,674 |

| adj.R2 | 0.196 | 0.617 | 0.434 | 0.732 | 0.924 |

TFP: total factor productivity; LP: Levinsohn-Petrin.

Second, this study used the average DT level of peer firms in the same province and industry as an IV. The rationale is twofold. First, DT in building and real estate companies depends heavily on the digital infrastructure of their location, as local technological environments provide essential support[7]. Additionally, collaborative upgrading within regional industry clusters creates competitive pressure, prompting building and real estate companies to integrate into the digital ecosystem to maintain core competitiveness. Therefore, the digital development level of the same industry in the same region is closely correlated with the DT level of individual companies[55], satisfying the relevance condition of the IV. Second, due to significant disparities in the efficiency of digital absorption and application across firms, the DT levels of the same industry in the same region do not directly affect their NQPFs[55], satisfying the exogeneity condition of the IV. Following Xiao et al.[55], this study used the annual mean DT level of peer firms in the same province and industry as the IV, Digital_Average. Columns (3) and (4) of Table 5 present the estimation results, both confirming the core conclusion of this study.

4.3.3 DID method

To further verify the effect of DT on NQPFs and address potential endogeneity bias in the baseline regression, this study used the “Broadband China” strategy as a quasi-natural experiment and applied the DID method for in-depth testing. By comparing performance differences between demonstration and non-demonstration cities before and after the policy shock, this method effectively eliminates common time trends and mitigates the influence of reverse causality on the estimation results. The “Broadband China” policy aimed to promote coordinated regional broadband network development, accelerate network optimization and upgrading, and improve application levels. This strategy has yielded significant results: on one hand, it fostered urban digital development in China[78]; on the other, it laid a crucial foundation for digital activities in building and real estate companies[79], significantly boosting local DT[55]. Following Zhao et al.[80], the variable Broadband was assigned a value of 1 for companies located in demonstration cities during and after the designation year, and 0 otherwise. Column (5) of Table 5 presents the corresponding regression results. The coefficient of Broadband is significantly positive at the 1% level, indicating that the establishment of these demonstration cities significantly drove the growth of NQPFs in local building and real estate companies.

4.4 Robustness tests

4.4.1 Alternative measures of NQPFs

This study re-estimated TFP using ordinary least squares, fixed effects, and generalized method of moments as proxies for NQPFs. Additionally, to account for the potential lagged effects of DT on NQPFs, the study re-estimated the regression models using one-period and two-period lagged values of NQPFs as dependent variables. The results, presented in Table 6, consistently confirm the main conclusions of this study.

Table 6. Alternative measures of new quality productive forces.

| Variables | (1) | (2) | (3) | (4) | (5) |

| TFP_OLS | TFP_FE | TFP_GMM | L1_TFP_LP | L2_TFP_LP | |

| Digital | 0.012*** (0.004) | 0.012*** (0.004) | 0.013*** (0.004) | 0.013*** (0.004) | 0.014*** (0.005) |

| Controls | YES | YES | YES | YES | YES |

| Firm | YES | YES | YES | YES | YES |

| Year | YES | YES | YES | YES | YES |

| Observations | 1,714 | 1,714 | 1,714 | 1,490 | 1,270 |

| adj.R2 | 0.938 | 0.945 | 0.830 | 0.928 | 0.894 |

OLS: ordinary least squares; FE: fixed effects; GMM: generalized method of moments; TFP: total factor productivity; LP: Levinsohn-Petrin.

4.4.2 Alternative measures of DT

Drawing on Wu et al. and Zhao et al.[8,17], this study constructed Digital_A and Digital_B. Digital_A was developed by selecting 76 feature words across five dimensions, including artificial intelligence, while Digital_B was based on 99 feature words from four dimensions, including digital technology applications. Both indices were calculated using term frequency analysis of the annual reports of Chinese A-share listed building and real estate companies. The regression results, presented in columns (1) and (2) of Table 7, are consistent with the conclusions outlined earlier.

Table 7. Alternative measures of digital transformation and subsample regression.

| Variables | (1) | (2) | (3) | (4) |

| TFP_LP | TFP_LP | TFP_LP | TFP_LP | |

| Digital_A | 0.011*** (0.003) | |||

| Digital_B | 0.004*** (0.001) | |||

| Digital | 0.011*** (0.004) | 0.017*** (0.005) | ||

| Controls | YES | YES | YES | YES |

| Firm | YES | YES | YES | YES |

| Year | YES | YES | YES | YES |

| Observations | 1,743 | 1,743 | 1,207 | 1,172 |

| adj.R2 | 0.914 | 0.914 | 0.915 | 0.917 |

TFP: total factor productivity; LP: Levinsohn-Petrin.

4.2.3 Subsample regression

First, due to the impact of the 2015 Chinese stock market crisis and the global COVID-19 pandemic (2020-2022) on the NQPFs of building and real estate companies, which hindered their DT progress, this study excluded observations from these four years and re-estimated the regression models. Second, given the unique political and economic status of municipalities directly under the central government and their specific policy preferences, the DT and NQPFs characteristics in these municipalities may differ significantly. Therefore, this study re-estimated the model after excluding observations from these municipalities. The regression results, presented in columns (3) and (4) of Table 7, show that the coefficient of DT remains statistically significant at the 1% level, consistent with the baseline findings.

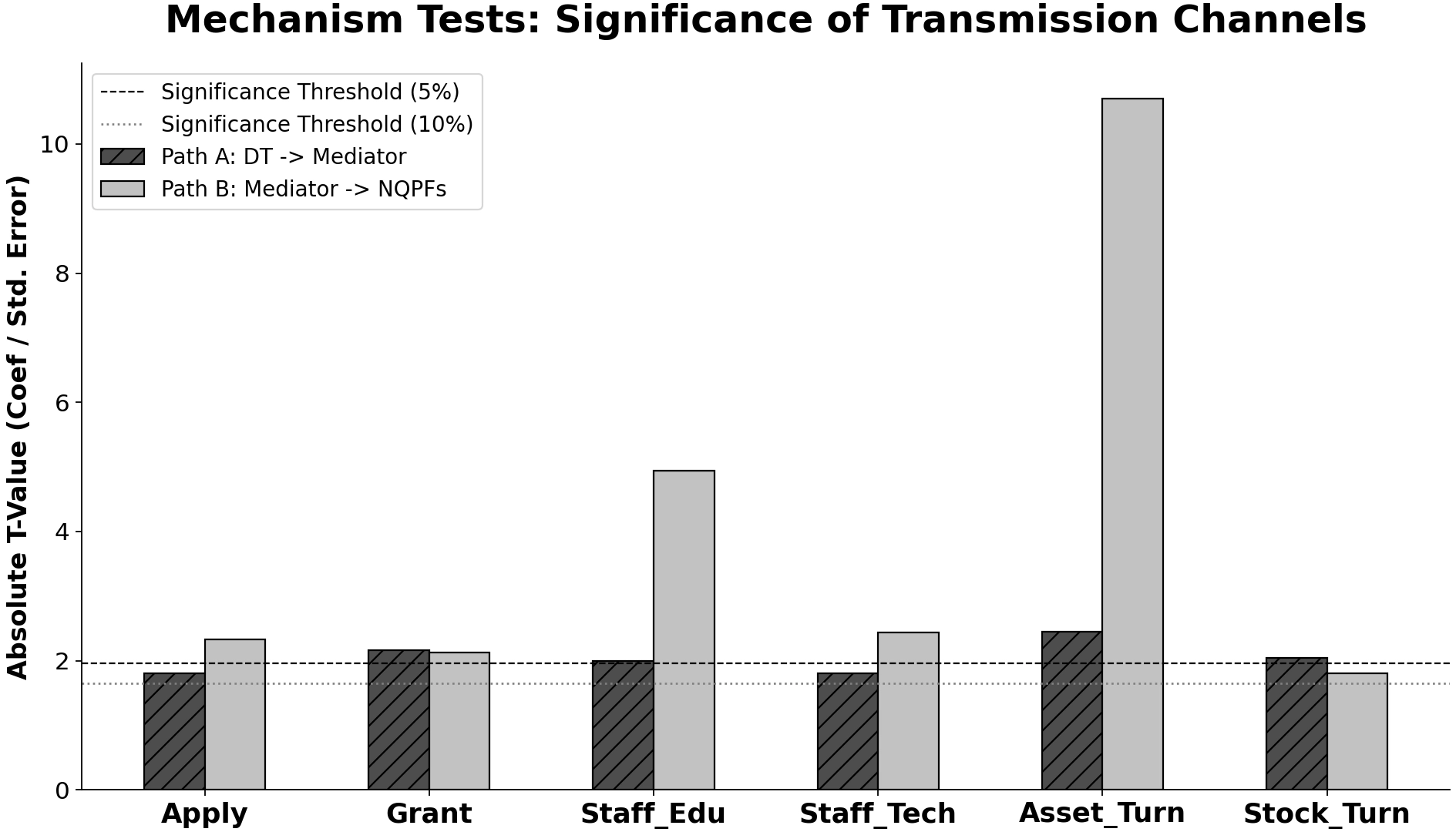

4.5 Mechanism tests

As discussed earlier, DT significantly improves the NQPFs of building and real estate companies; however, the underlying transmission mechanisms require further exploration. Consistent with the theoretical hypotheses of this study, DT enhances NQPFs in building and real estate companies by boosting innovation capacity, optimizing the human capital structure, and improving asset operational efficiency. This study developed mechanism effect test models, Equations (2) and (3), based on the baseline model, Equation (1). Here, Mediatori,t denotes the mediating variable, with detailed definitions provided below.

4.5.1 Innovation-driven mechanism

Building on the preceding analysis, DT enhances NQPFs in building and real estate companies by improving innovation capability. Following Guo et al.[75], this study used the natural logarithm of the number of patent applications (Apply) and the number of patents granted (Grant) in the current year to measure innovation capability. The number of patent applications reflects the level of innovation input, while the number of patents granted indicates the effectiveness of innovation output. The mediation effect test results are presented in Table 8. Columns (1) and (3) report the regression results of Equation (2), showing that the coefficients of Digital on the mediating variables Apply and Grant are significantly positive, indicating that DT enhances the innovation capability of building and real estate companies. Columns (2) and (4) report the regression results of Equation (3), which show that the coefficients of Apply and Grant on NQPFs are significantly positive. Crucially, after incorporating these mediating variables, the direct effect coefficients of Digital on NQPFs remain significantly positive (0.013 in Column 2 and 0.007 in Column 4). This confirms that the innovation-driven mechanism plays a significant partial mediating role between DT and NQPFs. These results support the aforementioned Hypothesis 2.

Table 8. Innovation-driven mechanism.

| Variables | (1) | (2) | (3) | (4) |

| Apply | TFP_LP | Grant | TFP_LP | |

| Digital | 0.009* (0.005) | 0.013** (0.006) | 0.013** (0.006) | 0.007* (0.004) |

| Apply | 0.091** (0.039) | |||

| Grant | 0.068** (0.032) | |||

| Controls | YES | YES | YES | YES |

| Firm | YES | YES | YES | YES |

| Year | YES | YES | YES | YES |

| Observations | 496 | 496 | 663 | 663 |

| adj.R2 | 0.961 | 0.935 | 0.949 | 0.947 |

TFP: total factor productivity; LP: Levinsohn-Petrin.

4.5.2 Human capital mechanism

The theoretical analysis of this study suggests that DT enhances NQPFs in building and real estate companies by optimizing the human capital structure. Following Huang et al.[7], this study measured the human capital structure from the perspectives of employee education level and functional type. First, the variable Staff_Edu was constructed, measured as the proportion of employees with a bachelor’s degree or higher. Second, employees were categorized into six major functions: production, administration, technology, marketing, finance, and others, with the proportion of technical staff used to create the variable Staff_Tech. The mediation effect test results are presented in Table 9. In columns (1) and (3), the coefficients of Digital on the mediating variables Staff_Edu and Staff_Tech are significantly positive, indicating that DT optimizes the human capital structure of building and real estate companies. In columns (2) and (4), the coefficients of the mediating variables Staff_Edu and Staff_Tech on NQPFs are significantly positive. Crucially, after incorporating these mediating variables, the direct effect coefficients of Digital on NQPFs remain significantly positive (0.009 in Column 2 and 0.010 in Column 4). This demonstrates that the optimization of the human capital structure plays a significant partial mediating role between DT and NQPFs. These results support the aforementioned Hypothesis 3.

Table 9. Human capital mechanism.

| Variables | (1) | (2) | (3) | (4) |

| Staff_Edu | TFP_LP | Staff_Tech | TFP_LP | |

| Digital | 0.002** (0.001) | 0.009** (0.004) | 0.003* (0.002) | 0.010** (0.004) |

| Staff_Edu | 1.029*** (0.208) | |||

| Staff_Tech | 0.391** (0.160) | |||

| Controls | YES | YES | YES | YES |

| Firm | YES | YES | YES | YES |

| Year | YES | YES | YES | YES |

| Observations | 1,566 | 1,566 | 1,566 | 1,566 |

| adj.R2 | 0.793 | 0.923 | 0.716 | 0.918 |

TFP: total factor productivity; LP: Levinsohn-Petrin.

4.5.3 Asset operation mechanism

Building on the preceding analysis, DT enhances NQPFs in building and real estate companies by improving asset operational efficiency. Following Li et al.[79], this study used total asset turnover (Asset_Turn) and inventory turnover (Stock_Turn) as indicators of asset operational efficiency. The mediation effect test results are presented in Table 10. In columns (1) and (3), the coefficients of Digital on the mediating variables Asset_Turn and Stock_Turn are significantly positive, indicating that DT improves total asset turnover and inventory turnover, thereby enhancing asset operational efficiency in building and real estate companies. In columns (2) and (4), the coefficients of the mediating variables Asset_Turn and Stock_Turn on NQPFs are significantly positive. Crucially, after incorporating these mediating variables, the direct effect coefficients of Digital on NQPFs remain significantly positive (0.010 in Column 2 and 0.015 in Column 4). This demonstrates that asset operational efficiency plays a significant partial mediating role between DT and NQPFs. These results support the aforementioned Hypothesis 4. The regression results for the mechanism analysis are presented in Figure 2.

Figure 2. Schematic diagram of mechanism analysis results. DT: digital transformation; NQPFs: new quality productive forces.

Table 10. Asset operation mechanism.

| Variables | (1) | (2) | (3) | (4) |

| Asset_Turn | TFP_LP | Stock_Turn | TFP_LP | |

| Digital | 0.004** (0.001) | 0.010** (0.004) | 1.256** (0.616) | 0.015*** (0.005) |

| Asset_Turn | 1.756*** (0.164) | |||

| Stock_Turn | 0.001* (0.001) | |||

| Controls | YES | YES | YES | YES |

| Firm | YES | YES | YES | YES |

| Year | YES | YES | YES | YES |

| Observations | 1,438 | 1,438 | 1,454 | 1,454 |

| adj.R2 | 0.856 | 0.943 | 0.438 | 0.919 |

TFP: total factor productivity; LP: Levinsohn-Petrin.

4.6 Heterogeneity analysis

4.6.1 Regional distribution

The spatial disparities in economic development and resource endowments in China may create a “digital divide” in the empowering effect of DT on NQPFs. Building and real estate companies across different regions face distinct market environments, technological ecosystems, and levels of policy support. Following the classification criteria from the National Bureau of Statistics, this study divided the sample into three sub-samples: Eastern, Central, and Western regions. Specifically, the variable Region was created to identify spatial location, assigning a value of 1 to the Eastern Region, 2 to the Central Region, and 3 to the Western Region. The regression results, presented in Table 11, reveal significant spatial heterogeneity. In column (1), the coefficient of Digital for the Eastern region is 0.015, significant at the 1% level, representing the strongest impact among the three groups. In column (2), the coefficient for the Central region is 0.009, significant at the 5% level. However, in column (3), the coefficient for the Western region is 0.004 and fails to pass the significance test. These results demonstrate that DT significantly enhances NQPFs in building and real estate companies in the Eastern and Central regions, while this effect is not yet evident in the Western region. This disparity can be attributed to the fact that the Eastern and Central regions possess more mature digital application scenarios, a higher concentration of high-tech talent, and more intense market competition, which collectively amplify the productivity gains from digital investments.

Table 11. Heterogeneity tests: Regional distribution.

| Variables | TFP_LP | ||

| (1) | (2) | (3) | |

| Eastern Region | Central Region | Western Region | |

| Digital | 0.015*** (0.005) | 0.009** (0.004) | 0.004 (0.006) |

| Controls | YES | YES | YES |

| Firm | YES | YES | YES |

| Year | YES | YES | YES |

| Observations | 748 | 451 | 356 |

| adj.R2 | 0.941 | 0.935 | 0.892 |

TFP: total factor productivity; LP: Levinsohn-Petrin.

4.6.2 Intellectual property protection

Higher levels of intellectual property protection allow building and real estate companies to benefit from exclusive rights to digital patents, facilitating the more efficient adoption of technological solutions and promoting NQPFs[7]. This study compared provincial intellectual property protection indices from the National Intellectual Property Administration’s “National Intellectual Property Development Status Report” with annual median values, creating two subsamples of companies with stronger and weaker intellectual property protection, and conducted grouped regression tests. The regression results, shown in columns (1) and (2) of Table 12, reveal that the coefficient of DT is significantly larger in the group with stronger intellectual property protection. This indicates that more robust intellectual property protection systems enhance the positive effect of DT on the NQPFs of building and real estate companies.

Table 12. Heterogeneity tests: Intellectual property protection and digital infrastructure.

| Variables | TFP_LP | |||

| (1) | (2) | (3) | (4) | |

| Stronger Intellectual Property Protection | Weaker Intellectual Property Protection | Better Digital Infrastructure | Poorer Digital Infrastructure | |

| Digital | 0.014*** (0.005) | 0.009 (0.007) | 0.015*** (0.005) | 0.014 (0.008) |

| Controls | YES | YES | YES | YES |

| Firm | YES | YES | YES | YES |

| Year | YES | YES | YES | YES |

| Observations | 829 | 795 | 1,137 | 200 |

| adj.R2 | 0.930 | 0.915 | 0.931 | 0.927 |

TFP: total factor productivity; LP: Levinsohn-Petrin.

4.6.3 Digital infrastructure

The DT of building and real estate companies depends on the digital infrastructure of their local ecosystem, as local technological environments provide essential support. Following Yang and Jiang[76], this study used the annual median value of the ratio of internet broadband access ports to the resident population in the provinces where building and real estate companies are located to classify the advancement of local digital infrastructure for grouped tests. The regression results, shown in columns (3) and (4) of Table 12, reveal that the coefficient of DT is significantly higher in the group with better digital infrastructure. This suggests that high-quality digital infrastructure amplifies the positive effect of DT on the NQPFs of building and real estate companies.

4.6.4 Ownership type

On the one hand, state-owned companies, benefiting from policy support, have significant advantages in accessing data factors and advanced technologies. On the other hand, due to soft budget constraints and inherent credit advantages, state-owned companies exhibit greater patience in long-term DT investments, enabling them to focus on high-risk, long-cycle innovation, thereby more effectively driving NQPFs growth. This study conducted grouped tests based on whether the controlling entity was state-owned. The regression results, presented in columns (1) and (2) of Table 13, reveal that the coefficient of DT is significantly higher in the state-owned enterprise group. This suggests that DT in state-owned building and real estate companies has a more pronounced positive effect on NQPFs.

Table 13. Heterogeneity tests: Ownership type and firm size.

| Variables | TFP_LP | |||

| (1) | (2) | (3) | (4) | |

| State-owned Enterprises | Non-state-owned Enterprises | Large Enterprises | Small and Medium Enterprises | |

| Digital | 0.024*** (0.007) | 0.002 (0.005) | 0.016*** (0.004) | 0.003 (0.007) |

| Controls | YES | YES | YES | YES |

| Firm | YES | YES | YES | YES |

| Year | YES | YES | YES | YES |

| Observations | 814 | 859 | 794 | 913 |

| adj.R2 | 0.921 | 0.906 | 0.934 | 0.843 |

TFP: total factor productivity; LP: Levinsohn-Petrin.

4.6.5 Firm size

On the one hand, economies of scale reduce marginal costs in DT investments for large companies and enhance the synergistic effects of massive data factors. On the other hand, the integration of mature R&D systems, supply chain networks, and other complementary assets with DT creates a multiplier effect, driving chain-wide collaborative innovation and facilitating a leap in NQPFs in both quality and efficiency. Following Huang et al.[7], this study used the natural logarithm of the number of employees to measure the size of building and real estate companies, compared this value with the annual industry median to determine firm size, and conducted grouped regression tests accordingly. The regression results, shown in columns (3) and (4) of Table 13, reveal that the coefficient of DT is significantly higher in the large enterprise group. This suggests that DT in large building and real estate companies has a more pronounced positive effect on NQPFs. The comparison of the aforementioned baseline regression and heterogeneity test results is shown in Figure 3.

Figure 3. Comparison of baseline regression and heterogeneity test results. DT: digital transformation; NQPFs: new quality productive forces.

4.7 Discussion

The empirical evidence from this study provides a nuanced resolution to the digital-era “Solow Paradox” within the context of China’s traditional, capital-intensive building and real estate sector. While previous literature presents mixed results on whether the adoption of new technologies consistently enhances productivity across general industries, our findings offer strong confirmation that DT effectively mitigates productivity stagnation in this specific sector. This shows that when digital technologies are deeply integrated into the core operational processes of asset-heavy enterprises, they shift from being mere capital expenditures to becoming pivotal engines driving the “novelty” and “quality” inherent in NQPFs.

Furthermore, our exploration of transmission mechanisms systematically unpacks the “black box” of digital empowerment. The results show that DT enhances NQPFs not through a single pathway, but rather through a structural reorganization of corporate resources. First, the innovation-driven mechanism demonstrates that digital tools (e.g., big data and cloud computing) reduce R&D barriers and foster cross-domain technological synergies. Second, the human capital mechanism provides empirical support for the “technology substitution and complementarity” hypothesis. By simultaneously eliminating routine, low-skilled tasks and creating a demand for non-routine, high-skilled digital talent, DT fundamentally upgrades the labor structure. Third, the asset operation mechanism highlights that real-time data flow and intelligent management systems optimize resource allocation, showing that DT can significantly streamline traditionally bulky supply chains in real estate enterprises.

Crucially, our multidimensional heterogeneity analysis reveals the boundary conditions of this digital dividend, emphasizing that the empowering effect of DT is highly context-dependent. The significant spatial disparities where DT empowers NQPFs in the Eastern and Central regions but is less effective in the Western region, support the existence of a regional “digital divide”. This suggests that the translation of digital investment into NQPFs requires a complementary ecosystem characterized by mature application scenarios and intense market competition. Similarly, the amplifying effects of strong intellectual property protection and advanced digital infrastructure highlight that digital empowerment depends heavily on a supportive institutional and physical macro-environment. Finally, at the organizational level, state-owned enterprises and large firms are better positioned to reap digital dividends. This is due to their advantages in resource availability, risk tolerance, and access to data, enabling them to bear the high sunk costs of foundational DT and achieve economies of scale in digital networks.

5. Conclusions

DT drives a new wave of factor and structural changes, enabling micro-level companies to enhance quality, efficiency, and undergo transformation. While most scholars support the positive effect of DT on socio-economic development, concerns about the “Solow Paradox”—where technological investments fail to translate into productivity gains—persist, particularly in traditional sectors. Focusing on the building and real estate industry, this study uses Chinese A-share listed building and real estate companies from 2011 to 2024 as the sample to investigate the effect of DT on the NQPFs of these firms. The findings, which provide fresh insights compared to existing literature, are threefold: First, DT significantly enhances NQPFs in building and real estate companies. Unlike prior studies that focused mainly on general industries and yielded divergent views on the “Solow Paradox”, our results confirm that DT successfully resolves this productivity paradox in traditional, capital-intensive sectors. This finding shows strong statistical and economic significance. Second, in terms of transmission mechanisms, contrary to previous research that broadly linked productivity gains to general technological progress, our results offer a more nuanced understanding specific to this industry. DT enhances NQPFs in building and real estate companies by boosting innovation capacity, optimizing human capital, and improving asset operational efficiency. Third, extending the limited boundary condition analysis in prior studies, this study demonstrates that, regionally, DT significantly enhances NQPFs in the Eastern and Central regions. Moreover, external factors like intellectual property protection and digital infrastructure, as well as internal conditions such as state ownership and large firm size, amplify this positive effect.

The principal contributions of this study are outlined as follows. First, by focusing on the building and real estate industry and precisely identifying the link between DT and NQPFs through empirical analysis, this study expands research on the economic effects of DT and the factors influencing NQPFs. It resolves the practical challenge of the “Solow Paradox” in this sector, offering theoretical guidance for DT and the sustainable growth of these companies. Second, as DT deeply integrates with production efficiency in building and real estate companies, this study clarifies three key transmission mechanisms: innovation-driven incentives, human capital, and asset operation. It unpacks the mechanisms linking DT and NQPFs, explaining how companies benefit from DT. Finally, by incorporating both external environments and internal conditions into the empirical analysis and examining their differential impacts, this study provides new empirical evidence for digital economy and NQPFs theories. It offers a basis for decision-making in implementing DT in building and real estate companies and formulating NQPFs development policies for the government, showcasing significant theoretical innovation and practical insights.

This study contributes to the literature on the digital economy and corporate NQPFs in three key areas. First, it extends the theoretical scope of the “Solow Paradox” by applying it to the building and real estate industry. While prior literature presents mixed results regarding the IT productivity paradox in general industries, this research provides compelling evidence that DT effectively mitigates productivity stagnation in traditional, capital-intensive sectors. Second, it develops a micro-level framework for enhancing NQPFs. Moving beyond direct effects, this study delineates how DT drives value creation through three specific channels: innovation capacity, human capital structure, and asset operational efficiency. This clarifies the theoretical mechanisms of internal factor reorganization in asset-heavy enterprises. Third, it systematically enriches the theory of boundary conditions for digital dividends. By incorporating multidimensional moderating variables, the study shows that the empowering effect of DT is contingent on spatial geography (with pronounced effects in the Eastern and Central regions), institutional environments (such as intellectual property protection and digital infrastructure), and organizational characteristics (ownership and size). This provides a more comprehensive theoretical framework for understanding the heterogeneous effects of DT.

Based on the empirical findings, this study offers several practical implications for policymakers and industry practitioners. At the policy level, digital development strategies should be customized to account for regional differences. Since DT significantly empowers firms in the Eastern and Central regions, policymakers could designate these areas as pilot zones for NQPFs initiatives. At the same time, targeted policy support should focus on the Western region to address the digital divide and enhance technology absorption capacity. At the industry level, industrial policies must foster the deep integration of digital technologies with sector-specific design and construction practices to drive NQPFs. For example, the adoption of prefabrication and modular construction, supported by Building Information Modeling (BIM) and digital twins, can substantially reduce material waste and carbon emissions, aligning directly with the green and sustainable goals of NQPFs. Additionally, deploying construction robotics for hazardous or repetitive on-site tasks not only enhances structural precision and operational efficiency but also promotes the workforce’s transition toward high-quality human capital. The integration of these technologies across core processes from architectural design to on-site assembly will help create specialized, high-productivity digital industry clusters within the building and real estate sector. At the institutional level, institutional and infrastructural environments must be optimized simultaneously to support sustainable digital empowerment. Strengthening the intellectual property protection system is crucial to safeguarding domain-specific digital innovations, particularly those involving technical assets such as proprietary algorithms used in smart building management systems. By optimizing lifecycle energy consumption and resource allocation, these smart systems will act as key drivers in enhancing operational NQPFs. Furthermore, upgrading network infrastructure to enable high-bandwidth 5G and Internet of Things connectivity will facilitate real-time construction site monitoring, seamless data synchronization, and automated quality control. By pairing these infrastructural improvements with reduced Industrial Internet access costs, systemic barriers to enhancing corporate NQPFs will be effectively lowered.

Although this study makes significant contributions, it has several limitations. First, DT is a dynamic and ongoing process, and its impact on the NQPFs of building and real estate companies evolves as technological penetration and industry dynamics change. This study focuses specifically on the period from 2011 to 2024 and does not fully capture this dynamic interaction process, resulting in an incomplete assessment of the long-term effects. Second, the study does not systematically distinguish between differences in business models, DT paths, and development stages across building and real estate companies. Additionally, it lacks a detailed exploration of subsectors such as residential development, commercial real estate, and construction, which limits the ability to provide specialized, targeted recommendations for companies. Future research could expand in three directions: First, by constructing regional-level DT indices and NQPFs indicators for the building and real estate industry, it would be possible to assess the overall influence of DT on industry development from a macro perspective. Second, future studies should delve deeper into the key driving factors influencing the DT of building and real estate companies, with a particular focus on identifying why some companies lead in the DT process. Lastly, more attention should be given to the application mechanisms of underlying digital technologies in DT, especially in specific contexts such as building modeling, project management, and intelligent marketing. A systematic analysis of their differentiated impact on the NQPFs of building and real estate companies would provide a stronger theoretical foundation for the sustainable growth of China’s building and real estate sector.

Acknowledgements

The authors are grateful to the anonymous reviewers for their valuable comments.

Authors contribution

Guo S: Data curation, formal analysis, writing-original draft.

Zhong Y: Conceptualization, methodology.

Conflicts of interest

The authors declare no conflicts of interest.

Ethical approval

Not applicable.

Consent to participate

Not applicable.

Consent for publication

Not applicable.

Availability of data and materials

Data supporting the findings of this study are available from the corresponding author upon reasonable request.

Funding

None.

Copyright

© The Author(s) 2026.

References

-

1. Huang H, Mbanyele W, Zhang L, Chen XL, Song M. Nonnegligible transition risks towards net-zero economy: Lessons from green finance initiatives in China. J Environ Manag. 2025;375:124132.[DOI]

-

2. Yu L, Zhang Q. Measurement of new qualitative productivity kinetic energy from the perspective of digital and green collaboration—Comparative study based on European countries. J Clean Prod. 2024;476:143787.[DOI]

-

3. Wang H, Zhou L, Liu X, Li H, Liu Y. Digital finance and new quality productive force of enterprise: Based on the analysis of enterprise industrial and commercial big data. Int Rev Financ Anal. 2025;104:104303.[DOI]

-

4. Chen Y. Improving market performance in the digital economy. China Econ Rev. 2020;62:101482.[DOI]

-

5. Bertani F, Ponta L, Raberto M, Teglio A, Cincotti S. The complexity of the intangible digital economy: An agent-based model. J Bus Res. 2021;129:527-540.[DOI]

-

6. Yoon S, Zhu H, Hwang BG, Min OS. Accelerating digital transformation in construction: Best practices for the successful implementation of integrated digital delivery. Autom Constr. 2025;178:106417.[DOI]

-

7. Huang B, Li HT, Liu JQ, Lei JH. Digital technology innovation and high-quality development of Chinese enterprises: Evidence from firm digital patents. Econ Res J. 2023;58(3):97-115. Chinese. Available from: https://kns.cnki.net/kcms2/article/abstract?v=_JlElU3EDUo1L1ZMsvyG4IwmWyKxw2q06HQOf_4Uf0wdSCE2WUsvCuEe-seljhK4KP0B3fiJzGLxL1FDM0KUlxIfe-O27k4FCNbAi4uqU-3k6OdxIptfolMfcs3YJgwfAjoCCMmO3EcJjhT5QAV4T7jWctrSlnM9JRlLNqffMef5wAki0UrLZAC8izDB50FtWlJyOQxHVb0&uniplatform=NZKPT&captchaId=6cf8ffa0-e75e-47dc-a256-7221caca1fea

-

8. Zhao CY, Wang WC, Li XS. How digital transformation affects enterprise total factor productivity. Finance Trade Econ. 2021;42(7):114-129. Chinese.[DOI]

-

9. Gong C, Ribiere V. Developing a unified definition of digital transformation. Technovation. 2021;102:102217.[DOI]

-

10. Firk S, Gehrke Y, Hanelt A, Wolff M. Top management team characteristics and digital innovation: Exploring digital knowledge and TMT interfaces. Long Range Plan. 2022;55(3):102166.[DOI]

-

11. He W, Ding Q, Zhou T. How fiscal policy drives corporate digital transformation: An analysis of the synergistic effects of tax incentives and special subsidies. Int Rev Econ Finance. 2025;103:104496.[DOI]

-

12. Xia K, Zhao L. Government procurement digitalization and corporate digital transformation: Evidence from China’s government procurement cloud platforms. Econ Anal Policy. 2026;89:21-34.[DOI]

-

13. Xie Y, Wu D. How does competition policy affect enterprise digitization? Dual perspectives of digital commitment and digital innovation. J Bus Res. 2024;178:114651.[DOI]

-

14. Chen Y, Pan X, Liu P, Vanhaverbeke W. How does digital transformation empower knowledge creation? Evidence from Chinese manufacturing enterprises. J Innov Knowl. 2024;9(2):100481.[DOI]

-

15. Wang J, Liu Y, Wang W, Wu H. How does digital transformation drive green total factor productivity? Evidence from Chinese listed enterprises. J Clean Prod. 2023;406:136954.[DOI]

-

16. Zhang R, Gao W, Chen S, Zhou L, Li A. Does digital transformation contribute to improving financing efficiency? Evidence and implications for energy enterprises in China. Energy. 2024;300:131271.[DOI]

-

17. Wu F, Hu HZ, Lin HY, Ren XY. Enterprise digital transformation and capital market performance: Empirical evidence from stock liquidity. Manag World. 2021;37(7):130-144. Chinese.[DOI]

-

18. Dou B, Guo S, Chang X, Wang Y. Corporate digital transformation and labor structure upgrading. Int Rev Financ Anal. 2023;90:102904.[DOI]

-

19. Huang Y. Digital transformation of enterprises: Job creation or job destruction? Technol Forecast Soc Change. 2024;208:123733.[DOI]

-

20. Zhang C, Qiu P, Zhang L, Hong X, Wang D. The impact of digital transformation on enterprises’ export stability: Evidence from listed companies in China. Int Rev Financ Anal. 2024;96:103582.[DOI]

-

21. Wang C, Wang D, Deng X, Wang S. Research on the impact of enterprise digital transformation on internal control. Sustainability. 2023;15(10):8392.[DOI]

-

22. Zhao Z. Digital transformation and enterprise risk-taking. Finance Res Lett. 2024;62:105139.[DOI]

-

23. Li S, Zhang X. Can digital transformation of enterprise improve the information environment of the capital market?—Evidence from Analyst’s perspective. Int Rev Econ Finance. 2025;97:103773.[DOI]

-

24. Leng A, Zhang Y. The effect of enterprise digital transformation on audit efficiency—Evidence from China. Technol Forecast Soc Change. 2024;201:123215.[DOI]

-

25. Cai C, Tu Y, Li Z. Enterprise digital transformation and ESG performance. Finance Res Lett. 2023;58:104692.[DOI]

-

26. Shen Y, Fu Y, Song M. Does digital transformation make enterprises greener? Evidence from China. Econ Anal Policy. 2023;80:1642-1654.[DOI]

-

27. Liu M, Li C, Wang S, Li Q. Digital transformation, risk-taking, and innovation: Evidence from data on listed enterprises in China. J Innov Knowl. 2023;8(1):100332.[DOI]

-

28. Wang X, Deng Y, Mao X. The impact of bank digital transformation on enterprises digital technology innovation in China. Int Rev Financ Anal. 2025;102:104068.[DOI]

-

29. Tang M, Liu Y, Hu F, Wu B. Effect of digital transformation on enterprises’ green innovation: Empirical evidence from listed companies in China. Energy Econ. 2023;128:107135.[DOI]

-

30. Peng Y, Tao C. Can digital transformation promote enterprise performance?—From the perspective of public policy and innovation. J Innov Knowl. 2022;7(3):100198.[DOI]

-

31. Su Y, Wu J. Digital transformation and enterprise sustainable development. Finance Res Lett. 2024;60:104902.[DOI]

-

32. Zhang X, Yue S, Tao J, Lai X. Does digital transformation affect corporate mergers and acquisitions? From the perspective of information asymmetry. Econ Anal Policy. 2025;86:764-778.[DOI]

-

33. Wu K, Fu Y, Kong D. Does the digital transformation of enterprises affect stock price crash risk? Finance Res Lett. 2022;48:102888.[DOI]

-

34. Chen J, Guo Z, Lei Z. Research on the mechanisms of the digital transformation of manufacturing enterprises for carbon emissions reduction. J Clean Prod. 2024;449:141817.[DOI]

-

35. Sun C, Zhang Z, Vochozka M, Vozňáková I. Enterprise digital transformation and debt financing cost in China’s A-share listed companies. Oecon Copernic. 2022;13(3):783-829.[DOI]

-

36. Chen G, Liu P, Jiang A. Does digital transformation in enterprises reduce debt default risk? Int Rev Econ Finance. 2024;96:103529.[DOI]

-

37. Pang S, Hua G. How does digital tax administration affect R&D manipulation? Evidence from dual machine learning. Technol Forecast Soc Change. 2024;208:123691.[DOI]

-

38. Zhu Y, Yu D. Digital transformation and firms’ bargaining power: Evidence from China. J Bus Res. 2024;183:114851.[DOI]

-

39. Geng Y, Zheng Z, Ma Y. Digitization, perception of policy uncertainty, and corporate green innovation: A study from China. Econ Anal Policy. 2023;80:544-557.[DOI]

-

40. Du Y, Li W, Tang X. Supply chain digitization and corporate maturity mismatch: Evidence from a quasi-natural experiment. Pac Basin Finance J. 2024;87:102514.[DOI]

-

41. Ma N, Zhang Z, Lan X, An K, Yang Y. How digital finance reduces corporate financial restatements: Evidence from China. Appl Econ. 2026;58(14):2634-2648.[DOI]

-

42. Zhu Z, Hua Q, Xu S, Lin W. The mechanism of green finance in promoting China’s new quality productive forces: Technological innovation and data factor. Res Int Bus Finance. 2025;79:103038.[DOI]

-

43. Chin T, Li Z, Huang L, Li X. How artificial intelligence promotes new quality productive forces of firms: A dynamic capability view. Technol Forecast Soc Change. 2025;216:124128.[DOI]

-

44. Ma S, Ding W, Liu Y, Zhang Y, Ren S, Kong X, et al. Industry 4.0 and cleaner production: A comprehensive review of sustainable and intelligent manufacturing for energy-intensive manufacturing industries. J Clean Prod. 2024;467:142879.[DOI]

-

45. Ren Y, Zhang J, Wang X. How does data factor utilization stimulate corporate total factor productivity: A discussion of the productivity paradox. Int Rev Econ Finance. 2024;96:103681.[DOI]

-

46. Li M, Wang Z, Wei Z. Digital new quality productivity and high-quality development of enterprises. Int Rev Financ Anal. 2026;109:104811.[DOI]

-

47. Jiang W, Li J. Digital transformation and its effect on resource allocation efficiency and productivity in Chinese corporations. Technol Soc. 2024;78:102638.[DOI]

-

48. Acemoglu D, Restrepo P. The race between man and machine: Implications of technology for growth, factor shares, and employment. Am Econ Rev. 2018;108(6):1488-1542.[DOI]

-

49. Ciarli T, Kenney M, Massini S, Piscitello L. Digital technologies, innovation, and skills: Emerging trajectories and challenges. Res Policy. 2021;50(7):104289.[DOI]

-

50. Li P, Zhao X. The impact of digital transformation on corporate supply chain management: Evidence from listed companies. Finance Res Lett. 2024;60:104890.[DOI]

-

51. Solow R. We’d better watch out. NY Times Book Rev. 1987;36:36. Available from: https://www.semanticscholar.org/paper/We%E2%80%99d-better-watch-out-Solow/cef149b3dbdaa85f74b114c2c7832982f23bcbf0

-

52. Brynjolfsson E, Rock D, Syverson C. Artificial intelligence and the modern productivity paradox: A clash of expectations and statistics. Natl Bur Econ Res. 2017.[DOI]

-

53. Yang L, Zhang Y, Huo B, Tian M. The impact of digital transformation on new quality productivity: A moderating analysis based on the socio-technical system theory. Ind Manag Data Syst. 2025;125(12):3179-3198.[DOI]

-

54. Chen ZS, Liang CZ, Xu YQ, Pedrycz W, Skibniewski MJ. Dynamic collective opinion generation framework for digital transformation barrier analysis in the construction industry. Inf Fusion. 2024;103:102096.[DOI]

-